Banks are testing a new type of crypto dollar called stablecoins. Here’s what that means for consumers

If you’ve ever sent money through Western Union, paid with a Visa card while traveling, or waited days for an electronic payment to settle, you’ve already used the systems known as “payment rails” that move money globally between friends, families and businesses.

Now, banks and payment companies are testing how cryptocurrency technologies might speed up those systems and help people process and reconcile payments more efficiently.

One of those tools is the , a type of digital designed to hold a consistent value. Stablecoins are most often pegged to the U.S. dollar (USD), but they can also be backed by other currencies, including fiat (government-issued) money and crypto.

Unlike other cryptocurrencies that can rise and fall sharply in price, USD-backed stablecoins are intended to remain, like their name suggests, predictable. As such, they’re designed for everyday transactions rather than trading and investing. explains how the introduction of stablecoins may affect consumers.

Why stablecoins are getting attention now

Interest in stablecoin technology has grown steadily over the past seven months, alongside clearer regulation. In July 2025, President Donald Trump signed the into law, which created a federal framework for certain dollar-backed digital crypto tokens. Regulators then opened 2026 by advancing and mulling over questions such as which regulatory body should oversee digital assets and how dollar-backed stablecoins could be used inside the banking system.

That regulatory momentum has made banks more willing to test the technology at scale, increasing the likelihood you’ll soon see stablecoins as an option at some checkouts. According to , stablecoin transaction volumes reached about $33 trillion in 2025, up from $19.7 trillion a year earlier, and the World Economic Forum that 2026 will be a “defining moment” for crypto technologies.

What is a stablecoin, and how do they work?

A stablecoin is a digital crypto token that represents a fixed amount of currency, most often one USD. Each is designed to track that value consistently because it’s backed by an equal amount of reserves held by the issuer, or the organization that creates and manages the stablecoin.

Stablecoins can be issued by banks, government-related entities, or private companies. The stablecoin issuer decides how many of the crypto coins will exist and holds the money or assets that back each token. Different issuers operate under different levels of oversight, and the rules for each are still being defined by lawmakers.

Still, issuers are responsible for following regulations, providing disclosures to customers, and maintaining systems that help keep the stablecoin’s value predictable.

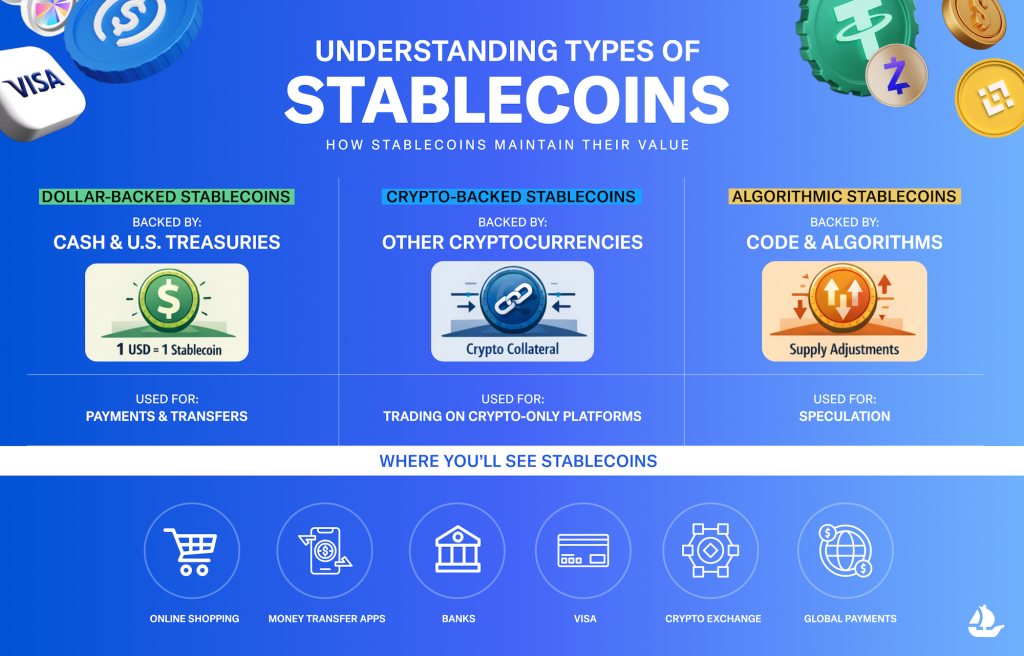

Types of stablecoins

“Not all stablecoins are created equal,” said Corey Ballou, head of trust and safety engineering at OpenSea. “The term covers a wide range of designs with very different risk profiles.”

The main difference between stablecoin types is the method used to maintain their value. Some stablecoins are issued by regulated entities and backed by reserves such as cash or short-term government securities, Ballou explained. Others rely on algorithms or market incentives to try to maintain a peg to the dollar.

“Those design choices matter,” Ballou said, “especially for consumers who may assume all stablecoins work the same way.”

Ballou explained users should understand how a stablecoin maintains its value before treating it as a payment tool or store of funds. Algorithmic stablecoins, in particular, can behave very differently during periods of market stress.

Dollar-backed stablecoins

This is the most common (and easiest to understand) kind of stablecoin. Each digital dollar is backed by real money or government assets, such as USD or Treasury bonds, held by the company or bank that issued it. The idea is that for every digital dollar in circulation, there is a real dollar or something very close to it set aside.

One example is USD Coin, known as , which is issued by , a U.S.-based financial technology company. Circle designed USDC to be used for payments, money transfers, and financial transactions. The company USDC is 100% backed by cash and “cash-equivalent assets” like short-term U.S. Treasuries.

Similar stablecoins also exist for other currencies, too, such as the euro (EUR). Fiat-backed stablecoins are the type most often used by banks, payment companies, government-related projects, and everyday consumers.

Crypto-backed stablecoins

Instead of being backed by cash, these stablecoins are backed by other cryptocurrencies. Computer programs help manage this process. Stablecoins in this category are more commonly used by traders who are familiar with crypto platforms than in traditional banking systems or payment apps.

One example is SkyDollar (), a stablecoin issued by . Formerly known as , Sky is a remote organization made up of users, developers, and investors, rather than a single issuer. The value of its stablecoin is collateralized by various cryptocurrencies. Because each cryptocurrency is valued differently, the group uses code to manage the system that maintains the stablecoin’s $1 value.

Algorithm-based stablecoins

These stablecoins are not backed by cash or crypto assets. Instead, they rely on software that automatically increases or decreases the number of tokens in circulation in an attempt to keep the price stable. Some of these systems have failed in the past, most notably the collapse of an algorithmic stablecoin known as TerraUSD (UST) in 2022, which and lost value.

Where consumers may see stablecoins

For most consumers, stablecoins are not expected to replace cash, credit cards, or bank accounts outright. Instead, banks, payment companies and online businesses are beginning to offer dollar-linked digital tokens as an additional way to pay for more flexibility. Stablecoins are already used in some online shopping checkouts, money transfer apps and cryptocurrency platforms, and they can sometimes settle faster and with lower fees than traditional payment rails.

What financial services are testing stablecoins?

Several large technology companies are testing stablecoins as a new way to send and receive money digitally. In January 2026, Polygon, one of the leading firms that builds crypto software, it would spend more than $250 million to buy two companies as part of an effort to introduce stablecoins to new consumers. One company operates a cryptocurrency exchange, or a marketplace where people can buy and sell digital tokens. The other builds crypto wallet software that allows consumers to store and use digital money in accounts that they own.

For most consumers, stablecoins are likely to appear inside apps and services they already use, rather than as a new type of money they need to seek out or manage. In financial apps such as Revolut, which an estimated to send money between international families and friends, stablecoins are now a currency option alongside traditional fiat currencies. Revolut in October 2025 that it would eliminate transaction fees for certain types of stablecoins, which could also make some of these peer-to-peer payments cheaper.

Meanwhile, Visa is to help businesses pay overseas suppliers, contractors or partners more quickly and at more convenient hours when banks in different time zones are closed.

In other cases, the decision to use stablecoins may be entirely up to the customer’s preference, with no need for the recipient to adjust their banking habits at all. Payments company Stripe, for instance, from customers who want to pay their invoices and subscriptions in crypto. Customers click “pay” as usual, but choose their stablecoin as the currency. The payments then settle in the business’s Stripe balance as USD like any other “normal” payment would.

Similarly, money-transfer apps like Zelle in October 2025 that it will begin testing the use of stablecoins in order to allow Zelle users to send money internationally. In the same month, Western Union, a company long known for international money transfers, a pilot for its own digital dollar token called USDPT. The token will be issued by Anchorage Digital Bank, a federally regulated digital asset bank, in the first half of 2026.

All this momentum has carried over into public currencies, too: In January 2025, Wyoming became the first U.S. state to , known as the , or , to test how digital dollars could be used for payments and the financing of public projects while staying within existing laws.

Finally, major banks including Bank of America, Citigroup, Goldman Sachs, Deutsche Bank, UBS, Barclays, Banco Santander, BNP Paribas, MUFG and TD Bank Group they are jointly exploring stablecoins tied to major national currencies such as the U.S. dollar, euro and Japanese yen, as they look for ways to move money faster using the underlying technology in a compliant way.

Are stablecoins safe for consumers?

Stablecoins are designed to be less volatile than other , but their safety for consumers depends on how they are issued, stored and used.

Beyond the type of stablecoin, Ballou said the way people use applications known as “digital wallets” can also play a major role in safety, sometimes even posing new opportunities for risk.

Only store in your crypto wallet what you’d be comfortable spending or, in a worst-case scenario, losing if hacked. “Think of a digital wallet like a payments app you’d use for everyday spending, not a place to store your entire savings,” Ballou said.

function more like payment apps than traditional bank accounts. One example is , a widely used app that lets people store and move digital assets. Interestingly, MetaMask has its own dollar-linked stablecoin, , that users can keep and send directly within the app.

Ballou added that starting with small amounts, keeping wallet software up to date, and using device-level protections such as passcodes or biometric locks can significantly reduce risk.

He also emphasized protecting recovery information that allows users to regain access to a wallet if they lose a phone or device. “Recovery phrases should be written down and stored offline in a secure location,” he said. “They shouldn’t be saved digitally and should never be shared with anyone.”

Finally, Ballou urged users to slow down before sending funds. “Taking an extra minute to verify transaction details before clicking send makes all the difference,” he said. “Users should double-check the destination address, the amount, the fees, and the asset before confirming a transaction.”

Used thoughtfully, stablecoins could help make payments faster and more flexible for consumers. Like any new technology, they also require new habits. Sticking to trusted apps and carefully reviewing details before sending money can help users take advantage of the benefits while reducing risk.

was produced by and reviewed and distributed by Â鶹Դ´.