10 financial vital signs to check each year, and the 3 most Americans ignore

Early in the year is a popular time to set financial goals and resolutions. But before you can plan where you want to go, it’s important to know where you’re starting from.

highlights financial vital signs that can help you assess your current financial situation and determine which areas may be worth setting goals in. Once you’ve done your financial health checkup, you’ll be well-prepared to set your financial goals for the new year.

Why Starting Your Financial Year With a Checkup Matters

A allows you to get a pulse on how your personal finances are doing. Have you made progress from last year? Are there any areas you’re really excelling in? Any that may need some extra attention?

Unfortunately, it’s a step that many people skip. A financial checkup offers plenty of key benefits, including helping you identify key problem areas and set your financial goals for the new year.

Once you’ve done a financial checkup, you may find that your financial stress is lower. You’ll feel more confident about where your finances sit today, as well as surer in your ability to reach your goals.

What a Financial Health Checkup Actually Is

Think of a financial health checkup like your annual checkup with your doctor. It’s a comprehensive review of every area of your , including your budget, savings, income, debt, insurance coverages, credit score, investments, estate plan, and taxes (along with anything else unique to your situation).

This financial checkup tells you where exactly your finances stand today, making it easy to see where you are compared to one year ago and compared to where you want to be.

For example, let’s say you do a financial health checkup every January. Maybe you do your checkup and see you have $15,000 in savings. You might feel discouraged if that’s less than your goal. But if you look back and see that you only had $5,000 in savings at this time last year, then you’ll feel confident and proud of your improvement.

In addition to helping you see how far you’ve come, your financial health checkup will show you problem areas that may need some extra attention this year.

Regardless of whether you have specific financial goals you’re reaching toward, it’s critical to annually to make sure you’re in a good place.

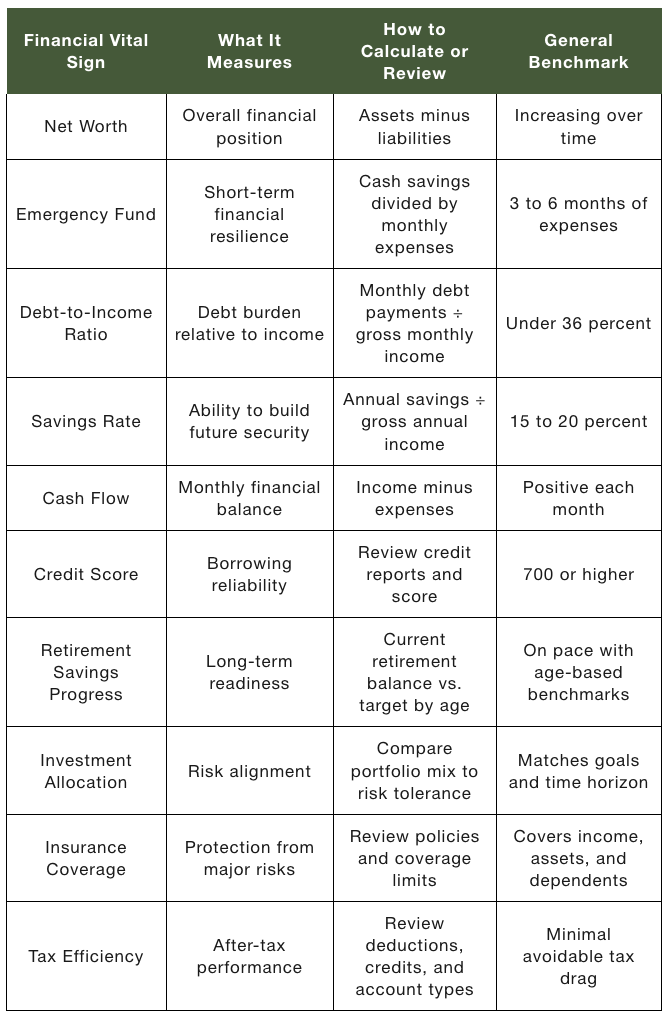

Core Financial Vital Signs to Measure

Many people aren’t sure where to start when assessing their financial health. There are 10 key vital signs to look at to help you get an idea of where your finances are.

1. Net Worth

Your net worth, which serves as a snapshot of your financial situation at a given point in time, is the difference between your assets and your liabilities (aka debts).

For example, let’s say you have $150,000 in your workplace 401(k) plan, another $80,000 in your individual retirement account (IRA), and $50,000 spread across other savings and investment accounts. On top of that, you own a home valued at $350,000. That brings your total assets to $630,000.

At the same time, you still owe $150,000 on your mortgage. You also have a car loan of $20,000, a student loan of $15,000, and around $7,500 of credit card debt. Your total liabilities equal $187,500.

When you subtract your liabilities from your assets, you’ll find you have a net worth of $442,500.

There’s not necessarily a specific net worth you should aim to have. Young people often start with a negative net worth if they took out student loans for college. The more important goal is that you see your net worth increase each year.

2. Emergency Fund Status

Your emergency fund is a pot of savings that’s available for emergency expenses, including job loss or unplanned expenses. This money can help keep you afloat if you lose some or all of your income. It can also help you navigate large emergency expenses without going into debt.

Experts generally recommend having at least three to six months of expenses in your emergency fund. If you’re in a dual-income household with no children and few financial obligations, you might feel comfortable saving just three months of expenses. On the other hand, if you have children and a mortgage and your family relies on your income, then a larger emergency fund is important.

3. Debt-to-Income Ratio

Your debt-to-income (DTI) ratio is the percentage of your gross income you spend on debt. It’s a tool that lenders use to assess whether you’re a good candidate for a loan, but you can also use it to assess whether you’ve overborrowed.

To calculate your DTI, divide your total monthly debt payments (including your mortgage, car loans, student loans, credit card payments, child support or alimony, etc.) by your gross monthly income (meaning your earnings before taxes and deductions).

If you have $3,500 of monthly debt payments and $10,000 of monthly income, your DTI is 35%, which is considered healthy. An ideal DTI is generally considered to be anything 36% or lower.

4. Savings Rate

Your savings rate is the percentage of your income you save each year. The higher your savings rate, the faster you’ll be able to reach your financial goals.

Experts generally recommend saving between 15% and 20% of your income, but that’s not possible for everyone at every life stage. Rather than focusing on the exact number, work on improving your savings rate each year, which you can do by either increasing your income or decreasing your expenses.

5. Budget Balance and Cash Flow

Your cash flow refers to all of the money coming into and out of your accounts. One of the easiest ways to track your household’s cash flow is to create a budget. Start by tracking where all of your money is going, then get more intentional about setting spending goals for each category.

It’s best to revisit your budget throughout the month to make sure you’re staying on track in each of your spending categories. But you can also revisit your budget each year to see trends in your income and spending, and decide whether your current spending goals still make sense.

In some cases, you may decide you need to cut back in certain areas, such as dining out or entertainment. On the other hand, you may decide you want to increase your spending in certain areas.

6. Credit Score and Report Review

Your credit report and credit score are two of the most important indicators of your financial health and affect your ability to borrow money, get affordable insurance, and even rent an apartment or get a job.

Your credit report is a detailed summary of your borrowing history, as reported to the credit bureaus by your lenders. Your credit score is a single number, ranging from 300 to 850, that essentially summarizes the health of your credit report. The higher your score, the better.

Reviewing your credit report annually is critical, as it can help you identify any errors on your credit report (if you find them, you should dispute them with the credit bureaus), as well as delinquent accounts that need addressing.

Federal law allows you to get a free credit report from each credit reporting company every year. You can request yours at

7. Retirement Savings Progress

Whether you’re in a workplace account like a 401(k) or in an IRA, it’s important to check in on your progress each year. Check your contribution rates to see how much you’re setting aside from each paycheck, and whether you can afford to increase that number.

At the very minimum, aim to contribute enough to earn your full employer match, which many companies offer as a percentage of your income. For example, your employer might offer to match your contributions up to 3% of your income, or match 50% of your contributions on the first 6% of your income.

In addition to checking your contribution rates, see how your is growing. You can’t control the performance of the market, but you can ensure your accounts are invested in such a way that aligns with your goals.

8. Investment Allocation

Your investment allocation refers to the way your money is divided up in your investment portfolio. It’s likely the money is divided up between stocks, bonds, and cash or cash equivalents. The ideal allocation varies depending on your age, your financial goals, and your risk tolerance.

If you’re in your 20s and plan to work until your 60s, you can afford to take a lot of risk in your portfolio. You’re probably invested primarily in stocks, with just a little bit in bonds and cash. On the other hand, if you’re just a few years from retirement, it’s likely a greater percentage of your portfolio is in bonds and cash, since you don’t want to risk losing it in the market.

A financial advisor can help run the numbers and find your ideal asset mix. Once you’ve found your ideal asset allocation, it will change over time. Additionally, you’ll need to rebalance your portfolio occasionally to make sure your portfolio still reflects your desired mix.

9. Insurance Coverage Adequacy

Insurance may be one of the least exciting aspects of personal finance, but it’s also one of the most important. Your insurance is what protects you when something goes wrong and helps ensure you get to keep your hard-earned savings.

The types of insurance you need may change over the years. Most people need health insurance, life insurance, and property insurance (either homeowners or renters), but you may also need to explore other types of insurance, including auto, disability, long-term care, umbrella, etc.

10. Tax Efficiency

Taxes are a fact of life, but there are steps you can take to legally lower your tax bill. You can review your tax efficiency yourself or work with a CPA who can review your situation.

As you’re reviewing your tax efficiency, make sure you review your current income and tax situation from the past year, understand what tax liabilities you might have in the new year (if you’re planning to sell some stocks, for example), or if there are any additional deductions you might be able to take advantage of.

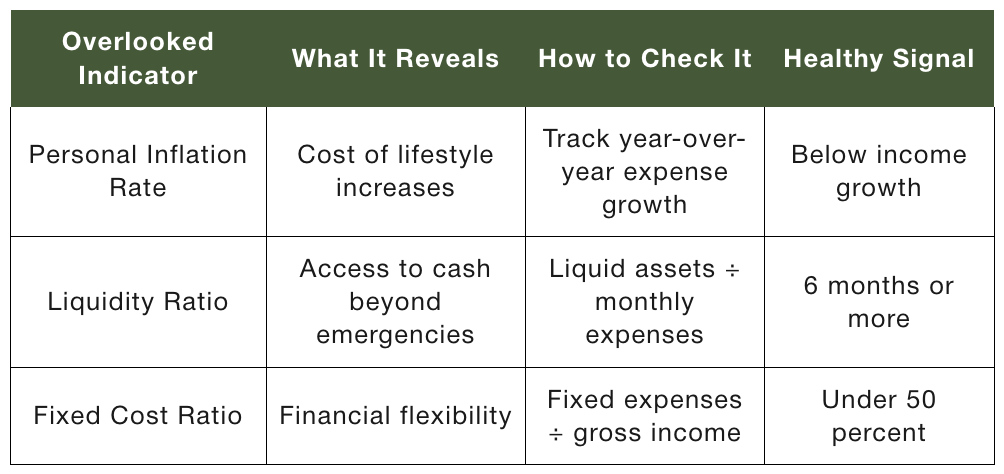

3 Financial Indicators Most People Ignore

The financial vital signs discussed above are the most important, and they’re also typically the ones people pay the most attention to. However, there are some other financial indicators that can help you assess your overall situation, but that most people ignore.

A. Personal Inflation Rate

Your personal inflation rate refers to how much your expenses rise each year (also known as lifestyle inflation). While the national inflation rate might be set at one number, your own spending may be rising more (or less).

It’s natural for your spending to increase as you age, especially as your income rises or as you enter more expensive phases of life, such as owning a home or having children. However, it’s important to make sure your spending is rising at a reasonable rate, and that it doesn’t exceed your income.

You can calculate your personal inflation rate by calculating how much higher your spending was in the most recent year than in the one before. Then, decide whether you’re comfortable with that number or whether you want to find ways to cut back in the coming year.

B. Liquidity Beyond Emergency Fund

An emergency fund is important, but that shouldn’t necessarily be the only liquid savings you have.

You’ll also want liquid savings for any other financial goals you’re working toward. You should generally use deposit accounts or low-risk investment accounts to save for your short-term goals, such as those happening within the next few years.

For example, if you’re buying a house next year, you’ll want that money in a savings account rather than in the stock market to ensure it doesn’t lose value before you need it.

Savings for financial goals that are further away can be less liquid, as you can afford to take a bit of risk with those dollars since you won’t be needing them anytime soon.

C. Fixed Cost Ratio

Your personal fixed cost ratio shows the percentage of your income you spend on your fixed costs (think your mortgage, utilities, insurance, transportation, childcare, etc.). The higher your monthly fixed costs, the less flexibility you have in your budget.

Depending on where you live and the stage of life you’re in, a high fixed cost ratio may be unavoidable. In most cases, someone living in New York City will have higher fixed costs than someone living in the Midwest. But there are steps you can take to free up more of your monthly income, such as increasing your earnings or finding ways to reduce your costs.

Financial Indicators Many People Overlook

How to Act on What You Find

Completing your financial checkup is only one piece of the puzzle. Once you’ve done that, you need to act on it. Based on what you find when checking in on your finances, you can probably clearly identify a few problem areas in your finances, whether it’s your credit score, your debt-to-income ratio, your budget, or something else.

Once you know which areas need your attention, you can set financial priorities and goals for the new year. Once you’ve set broad goals, narrow those down even more into a specific for each area you want to work on.

Financial Health FAQs

How often should you check your financial vital signs?

For most people, once per year is a good frequency for a financial checkup, with lighter reviews each quarter. You should track your income and spending monthly. There’s no best time of year to complete these checks, but January is often a good time before income resets, benefit elections are fresh, tax planning opportunities are still available, and people are already in goal-setting mode.

What is the most overlooked financial metric for most households?

Liquidity is often overlooked. Many people focus on net worth but fail to measure how quickly they can access cash during a disruption. Strong liquidity supports flexibility and reduces stress during unexpected events.

What should you do if several of your financial vital signs look unhealthy?

If you do a financial checkup and several of your vital signs look unhealthy, start by prioritizing those that affect your daily stability, such as your cash flow, emergency fund, and high-interest debt. Once you get those under control, you can start to address the longer-term issues, such as retirement savings. It’s impossible to fix everything at once, so it’s important to make a step-by-step plan.

Can you have a high income and still have poor financial health?

Yes, unfortunately, many people in the United States have high incomes, but are still struggling financially. Low savings rates and high spending result in even high earners living paycheck to paycheck. No matter what your income level is, there are steps you can take to improve your personal financial health one step at a time.

What financial vital signs matter most before retirement?

The most important financial vital sign on a day-to-day basis is your cash flow. Are you spending less than you’re bringing in? Are you saving at least some of your income? When you look at the big picture, your retirement savings progress, tax efficiency, and healthcare planning become especially relevant as retirement approaches. Reducing your debt and ensuring that your portfolio risk aligns with your financial goals can put you in the best position for retirement.

was produced by and reviewed and distributed by Â鶹Դ´.