7 tax moves to consider before the end of the year

As we approach the end of the year, it’s important to make sure your tax situation is in order. Many people don’t think about their taxes until spring, since tax returns aren’t due until April 15. But there are plenty of year-end tax moves you must make by December 31 for them to count toward this year.

To make sure you’re truly optimizing your taxes, explains how to assess your tax situation before the end of the year and make any last-minute tax moves that can help lower your tax bill in April and better set you up for the future.

TL;DR: 7 moves to do before December 31

- Max out your workplace and individual retirement plan contributions for 2025, including making any catch-up contributions you’re eligible for.

- Evaluate your tax situation to determine whether a Roth conversion is a good idea, and then make sure to complete the conversion by December 31.

- Harvest your tax losses to help lower your capital gains tax liability, but make sure to avoid wash sales.

- If you’re 73 or older, take your RMDs for the year. If you aren’t sure how much you’re required to take, use the IRS worksheet or an online RMD calculator.

- Use your FSA dollars by December 31 or, if your plan allows it, set your carryover strategy. Make sure to elect next year’s FSA deferrals while you’re at it.

- Check your tax withholding to make sure you’ve paid enough in income taxes for 2025. If you’ve underpaid your taxes, make an estimated tax payment to avoid penalties and interest.

- If applicable, make a 529 plan contribution by the end of the year to qualify for your state’s income tax deduction or credit.

1) Maximize retirement plan contributions

Each year, the IRS sets a maximum amount you can contribute to your tax-advantaged retirement accounts. The is $23,500 for 401(k) plans and $7,000 for individual retirement accounts (IRAs).

Both plans also allow for if you’re 50 or older. 401(k) investors can contribute an additional $7,500 once they reach age 50, and up to $11,250 for ages 60-63. For IRAs, the catch-up contribution for everyone 50 and older is $1,000.

Why it’s important

Retirement accounts come with major tax advantages that make them a more cost-effective option than investing in a standard taxable brokerage account. The more money you can put into these accounts each year, the better situated you’ll be for retirement.

Next steps to maximize your retirement contributions

If you’re not currently on track to max out your accounts, increase the percentage of your pay that’s automatically withdrawn from your paycheck to make sure you hit your goal.

We know not everyone can contribute the maximum amount. In that case, contribute as much as your budget will allow, or perhaps consider putting a year-end bonus toward your retirement accounts.

Pro tip: While the 401(k) contribution deadline for 2025 is December 31, the deadline for contributing to your IRA for this tax year isn’t until April 15. If you can’t afford to contribute extra to both right now, prioritize 401(k) contributions, and then work on beefing up your IRA between January 1 and April 15.

2) Consider a Roth conversion

A allows you to move money from your pre-tax IRA or 401(k) to a Roth account.

Roth accounts don’t come up with the upfront tax benefit that traditional retirement accounts do. You’ll pay taxes on the income you contribute to these accounts, but then you won’t pay taxes on your investment earnings or withdrawals. Contrast that with a traditional IRA or 401(k), which allows for pre-tax contributions, but then you’ll pay income taxes on your withdrawals.

If you convert money you’ve already taken a tax deduction for, you’ll have to pay taxes on the amount you convert. However, if you do the Roth conversion in the same year you contributed the funds, there likely won’t be any tax liability since you haven’t enjoyed the tax benefit yet.

Who a Roth conversion is best for

Anyone can use a Roth conversion, but it’s often best suited to lower-income earners. If your income (and, therefore, your tax rate) is lower today than it will be in the future, it’s often a better option to take the tax hit today with the Roth conversion, but then enjoy the tax break later when your income is higher.

Roth conversion timing and tax impact

You must complete your Roth conversion by December of the conversion year. If there’s a tax liability associated with the conversion, you’ll have to pay that when you file your 2025 tax return.

The timing is also important because you before you can take penalty-free withdrawals of money you convert from a traditional to a Roth account. If you complete your conversion by December 31 of this year, you can access those funds a full year earlier than if you waited until January.

3) Harvest tax losses, but mind the wash-sale rule

is a strategy where you sell investments at a loss to help offset some of your taxable gains. The losses offset the gains, which lowers your tax bill at the end of the year.

For example, let’s say you sold a stock from your portfolio for a gain of $1,000. Normally, you’d pay capital gains taxes on those earnings. Assuming you’re in the 15% capital gains tax bracket, you’d pay $150 in taxes. However, if you have another investment that’s down and you can sell it for a $1,000 loss, you’d completely eliminate the tax liability on your capital gain.

Be wary of the wash sale rule

The rule prohibits buying a “substantially identical” security within 30 days before or after a sale. For example, you wouldn’t be allowed to harvest your losses in Apple stock on a day when its stock price is down, immediately repurchase the stock, and claim the tax benefit of the loss.

If you decide to harvest your tax losses, make sure you wait at least 30 days before you repurchase the stock or choose a different stock that’s not substantially identical to purchase.

Deducting excess losses

Selling your losing investments can have tax benefits even if you don’t have capital gains to offset. The IRS allows you to above and beyond your capital gains, which can lower your overall tax bill.

If your excess losses are more than $3,000 (or you simply want to delay the tax benefit until you have gains to offset), you can carry them forward to future tax years.

4) Take your required minimum distributions

Everyone has to start taking from their pre-tax retirement accounts in the year they turn 73. This rule applies to 401(k)s, 403(b)s, 457(b)s, traditional IRAs, SEP IRAs, and SIMPLE IRAs. The only exception is that, if you’re still working, you don’t have to take RMDs from your workplace retirement plan.

Your RMD is based on your life expectancy and the balance of your retirement account. You can use a to calculate your RMDs, or you can use an online calculator, such as the one provided by the .

As a quick example, if your previous year-end account balance was $1 million and you’re 75 years old, you have a withdrawal factor of 24.6. You divide your account value by this number to find that you have an RMD of $40,650.41.

RMD penalties

If you don’t take your RMDs by the end of the year, you’ll pay an excise tax of 25% on the amount you failed to withdraw. If you correct the RMD within two years, you’ll only pay 10%.

Using Qualified Charitable Distributions to satisfy your RMDs

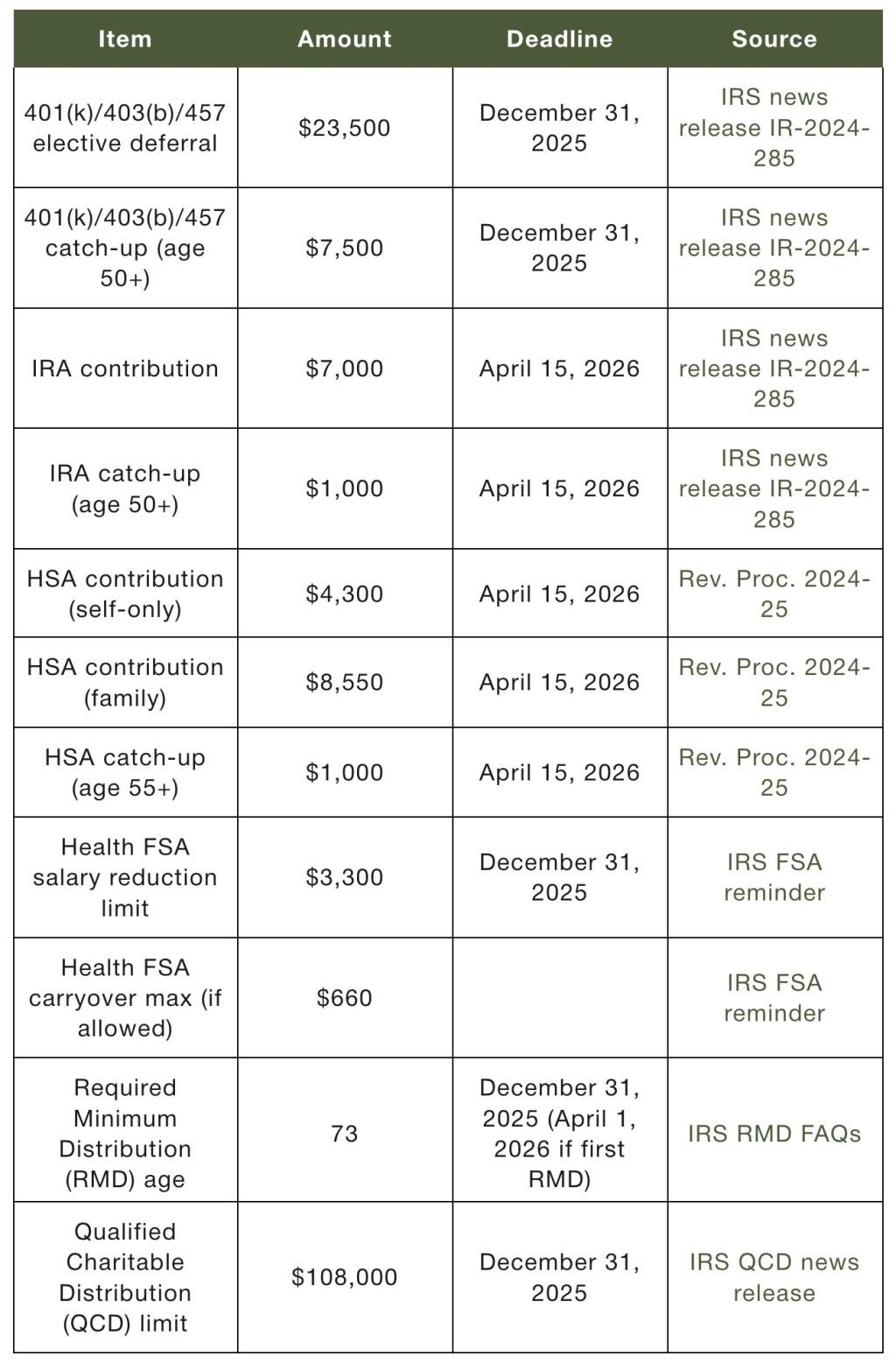

If you’d rather avoid the tax liability from your RMD, you can choose to of your RMD amount. The maximum QCD amount in 2025 is $108,000 per person.

An example of when a QCD might make sense is if you’re still working, don’t need the income from your RMD, and want to avoid the extra tax liability that comes with it. It could also make sense , but don’t need the additional income and want to pay less in taxes.

5) Use FSA funds and set next year’s election

Unlike health savings accounts (HSAs), which allow your money to grow in perpetuity, generally have a deadline of December 31 to use your funds. (though some plans give you until March 15).

You can use your FSA for any qualified medical expenses, including medications (prescription or over the counter), medical appointments, dental and eye appointments, medical equipment, personal care products, and more.

Make your FSA election for next year

Unlike with other tax-advantaged accounts, FSA elections don’t carry over from year to year. Even if you elected to contribute to an FSA last year through paycheck deferrals, you’ll have to re-make the election for the 2026 year.

6) Check withholding and, if needed, make an estimated payment

Before the end of the year, it may be a good idea to check your tax withholding and, if necessary, make an estimated tax payment.

If your income changes from year to year, your tax liability also changes. Among other things, this means you’re in danger of underpaying your taxes in a year when your income is higher. Luckily, the IRS provides a to help you estimate your federal income tax withholding and make sure you’re on track to pay enough in taxes.

Avoid an underpayment penalty

If you’re underpaying your taxes so far, you can make an estimated tax payment to go toward your 2025 taxes. The deadline for 2025 estimated tax payments is January 15, 2026. If you don’t make an estimated tax payment and you end up underpaying your taxes by more than $1,000, you could be .

7) Make your 529 plan contributions to get your state benefits

don’t have contribution deadlines in the same way as other accounts, nor do they have annual contribution limits. Your 529 plan contributions also aren’t deductible on your federal income taxes. However, there are still some reasons to revisit your contributions before the end of the year.

First, allow you to claim an income tax deduction or credit for your 529 contributions. So even though you can’t claim them on your federal taxes, they can help reduce your state income tax bill.

Additionally, contributing to a 529 plan, even for your own child, could trigger the gift tax. The gift tax exclusion for 2025 — meaning the amount you can give without having to file a gift tax return — is . Additionally, the IRS where you make a contribution of up to five years of 529 contributions at once without triggering a gift tax consequence.

2025 key numbers and dates (quick reference table)

Are you planning to use any of the strategies we’ve talked about in this guide before the end of the year? The table below breaks down some of the key numbers and dates you’ll need to know, including account contribution limits and deadlines.

FAQs

What is the deadline for most year-end tax moves?

The deadline for most year-end tax moves is either December 31 or April 15. You have until December 31 to take your RMDs (except your first one), do Roth conversions, make qualified charitable distributions, make 401(k) contributions, and spend your FSA dollars (in most cases). However, some moves can be made until April 15, including IRA contributions and HSA contributions.

What are the 2025 limits for 401(k)s, IRAs, HSAs, and FSAs?

The 2025 contribution limits for 2025 are $23,500 for 401(k) plans (plus an additional either $7,500 or $11,250 for catch-up contributions), $7,000 for IRAs (plus an additional $1,000 for catch-up contributions), $4,300 for individual HSAs or $8,550 for family HSAs (plus an additional $1,000 for catch-up contributions), and $3,300 for FSA contributions.

Do Roth conversions have a December 31 deadline?

Yes, Roth conversions must be completed by December 31, 2025 to count toward the 2025 tax year. If you wait until after the new year to make the conversion, it will count toward the 2026 tax year and you’ll have to wait an additional year before that money is accessible to you.

What’s the wash-sale window

The wash sale window is 30 days before and 30 days after (for a total of 61 days) the sale date. If you repurchase a substantially identical security within that timeframe, you’ll be in violation of the rule.

When do RMDs start and what’s the deadline?

RMDs (short for required minimum distributions) start the year you turn 73. You must take your first RMD by April 1 of the following year, but all subsequent RMDs must be taken by December 31.

Can a QCD satisfy my RMD?

Yes, a QCD (short for qualified charitable distribution) can satisfy your RMD requirement from an IRA. It will help you avoid taxation on your RMD, but it also requires giving the money away.

Talk with an advisor

If you’re trying to get your ducks in a row before the end of the tax year, consider speaking with a financial advisor. Everyone's situation is unique, and a financial advisor can look at yours and advise you on the best tax moves to make before the end of the year.

This guide about breaks down the different ways an advisor can help you with your tax optimization.

Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA. Investing involves risk, including possible loss of principal.

Prior to investing in a 529 Plan, investors should consider whether the investor’s or designated beneficiary’s home state offers any state tax or other state benefits such as financial aid, scholarship funds, and protection from creditors that are only available for investments in such state’s qualified tuition program. Withdrawals used for qualified expenses are federally tax free. Tax treatment at the state level may vary. Please consult with your tax advisor before investing. Investing involves risk, including possible loss of principal.

was produced by and reviewed and distributed by Â鶹Դ´.