How policy is setting the stage for markets in 2026

As we step into 2026, the fundamental backdrop for markets appears more favorable than anything weŌĆÖve seen since 2021. It may be hard to remember after wrapping up a strong year for global markets, but investors climbed a significant wall of worry throughout 2025. Policy uncertainty dominated headlines: Would DOGE trigger a recession? Was the U.S. heading into a trade war? Would the Fed prioritize fighting inflation or supporting the markets?

Many of these questions have been answered, and two powerful forces are now working in investorsŌĆÖ favor: policy clarity and Federal Reserve support. looks at the potential impact of policy on markets this year.

The Macro Reset: Policy Fog Has Lifted

Investors hate uncertainty more than they hate bad news. Throughout 2025, they faced three major policy unknowns that froze decision-making and weighed on markets. Now, they finally have answers.

The Fear of DOGE

Following the creation of the Department of Government Efficiency, headlines suggested a staggering $2 trillion in immediate spending cuts. Markets worried about the risk of ŌĆ£shock therapyŌĆØ that could trigger a government-induced recession.

The 2026 Setup: The U.S. endured some hiring freezes and increased scrutiny on government waste, but the catastrophic demand shock never arrived. DOGE quietly wound down in November 2025 and a ŌĆ£slash and burnŌĆØ approach to government spending is no longer a market concern.

The Tax Cliff

The looming expiration of the Tax Cuts and Jobs Act created a massive overhang at the beginning of 2025. CFOs froze spending plans and M&A slowed, as it was difficult to model returns on investment without knowing tax policy.

The 2026 Setup: The ŌĆ£One Big Beautiful Bill ActŌĆØ was enacted in July 2025, setting tax rates for the next several years. Businesses now have the visibility they need to unlock their balance sheets.

Tariff Russian Roulette

Perhaps the most traumatic policy risk of 2025 was trade rhetoric that seemed to escalate daily. Threats of 100% tariff rates became a regular occurrence, and investors feared an extreme universal tax that would reignite 1970s-style stagflation.

The 2026 Setup: Tariff-related fears briefly sent us into a bear market in 2025, but investors now recognize that tariff-related inflation is a manageable friction, not an existential risk to margins.

The Fed Has Shown Its Cards: Support, Not Restraint

Perhaps more than fiscal policy, valuations, or even earnings, a highly important variable for markets is the Federal Reserve. In 2026, the Fed appears ready to shift from fighting inflation to protecting expansion, acting as a powerful backer for markets.

For the first time since 2021, the Fed is using both of its primary tools to support asset prices:

1. Lowering Short-Term RatesŌĆŹ

The Fed cut rates three consecutive times through December, bringing the target range down to 3.5%-3.75%. This directly stimulates economic activity.

2. Ending Quantitative Tightening

Perhaps more importantly, the Fed quietly ended on Dec. 1. For two years, the Fed drained liquidity from the financial system every month by letting bonds roll off its balance sheet. It was a silent headwind for risk assets. By stopping this runoff, theyŌĆÖve removed a structural drag on markets.

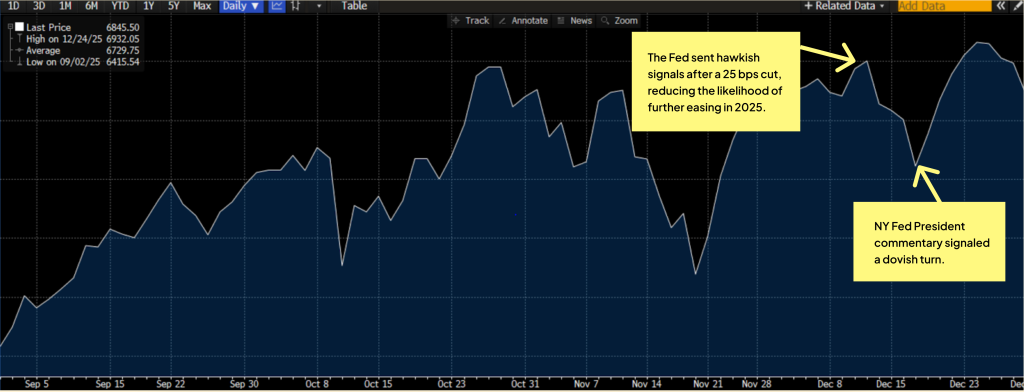

The Pivot: A Real-Time Case Study

The impact of the Fed on market performance is hard to overstate. When the Fed started to sound in late October, the Range investment team went on . The market proceeded to struggle for weeks. After a noticeable dovish in Fed-speak in late November, the markets were able to resume their upward trajectory.

The 2026 Setup: In 2025, the Fed was still a gatekeeper, curtailing risk. In 2026, the Fed is likely to be an enabler. With the ŌĆ£inflation emergencyŌĆØ declared over, the central bankŌĆÖs bias has shifted toward supporting the expansion.

The Outlook For 2026 ŌĆö A ŌĆśRisk OnŌĆÖ Backdrop

With clarity comes confidence. 2026 may be the year when the tangible benefits of a more pro-business policy mix show up in the data and support a broader universe of stocks. The ŌĆ£animal spiritsŌĆØ many expected in 2025 may finally emergeŌĆösupported by policy clarity and a Federal Reserve that has shifted from restraint toward accommodation.

This could translate into two supportive dynamics:

1. Wider Market Participation (Increased Breadth)ŌĆŹ

While megacaps drove index performance, the average U.S. company has struggled to grow earnings and invest with conviction. A key reason has been uncertainty: When tax policy and trade rules are moving targets, CFOs raise hurdle rates, delay capex, and keep balance sheets defensive. As that fog lifts, the beneficiaries should extend well beyond AI-linked winnersŌĆöand toward the broader universe of domestic cyclicals, industrials, financials, and services businesses that are most sensitive to planning certainty.

Monetary policy also works with a lag, and in 2026, corporations may feel the benefit of roughly 175 bps of cumulative rate cuts delivered since the easing cycle began. Further easing also seems likelyŌĆöespecially if we lap tariff impacts after Q1 and AI-driven productivity gains help keep inflation contained. Lower rates benefit small- and mid-cap stocks disproportionately, given higher leverage, greater cyclicality, and a heavier dependence on domestic demand.

2. Supported Valuations

Markets should benefit from an easing liquidity headwind as quantitative tightening by the Fed has ended. A less restrictive liquidity backdrop typically lowers the ŌĆ£hurdle rateŌĆØ investors apply to future cash flows and reduces the extra return they demand to own equities. That doesnŌĆÖt guarantee higher P/E multiples, but it does raise the floor under valuationsŌĆömaking it easier for stock prices to hold through normal growth or inflation noise.

Keep in mind, policymakers do not have a blank check to remain accommodative. They must maintain credibility, and the bond market will continue to act as a ŌĆ£governorŌĆØ on monetary and fiscal policy. If yields spike aggressively, equity valuations will face pressure. But for now, it appears the chosen path for both lawmakers and the Fed is to enable, rather than curtail, the economic expansion.

Disclosures:

This communication contains forward-looking statements that reflect Range Advisory, LLCŌĆÖs (ŌĆ£RangeŌĆØ) current views, expectations, beliefs and/or projections about future events or results. Forward-looking statements involve risks and uncertainties ŌĆö including, without limitation, market conditions, regulatory changes, economic conditions ŌĆö any of which could cause actual results to differ materially from those expressed or implied by such statements. Range undertakes no obligation to update or revise any forward-looking statements to reflect new information, future events or otherwise, except as required by law. Recipients should not place undue reliance on forward-looking statements, which are presented for informational purposes only and do not constitute investment advice or a recommendation to buy, hold, or sell any security. Past performance is not indicative of future results. The views, opinions and analyses expressed by Range in this material are those of Range as of the date shown, and are provided for informational purposes only.

was produced by and reviewed and distributed by ┬ķČ╣įŁ┤┤.