It’s Financial Wellness Month: Are you prepared?

January is financial wellness month. That makes it the perfect time to work on improving financial habits, including saving more money, paying down bills, saving for retirement and life goals, and ensuring you and your family are protected from risks.

takes a closer look at what financial wellness means and how having sufficient insurance coverage can safeguard it.

What Financial Wellness Means for You

When most people think of “wellness,” they likely focus on good physical and mental health. But finances can have a wellness component, too, that is just as important to take stock of. Alarmingly, a 2024 Guardian Life report reveals that , the lowest level in 14 years.

“Financial wellness is really about having enough stability and breathing room so that a single unexpected event does not unravel years of hard work. Revisiting your financial wellness from time to time can help you catch gaps before they show up at the worst possible moment,” explains a Certified Financial Professional.

Ask , senior wealth counselor at Avenue Investment Management, and he’ll tell you that financial wellness implies having a liquid reserve of three to six months of expenses and trying to grow your total wealth faster than the rising cost of living.

With the turn of a calendar year and a focus on New Year’s resolutions, January is an ideal time to scrutinize your financial wellness, set goals, and strive for improvement in how you manage your dollars.

“People should reassess their financial position in January since cost increases and lifestyle modifications can change the trajectory of their long-term plans,” says Ferrara.

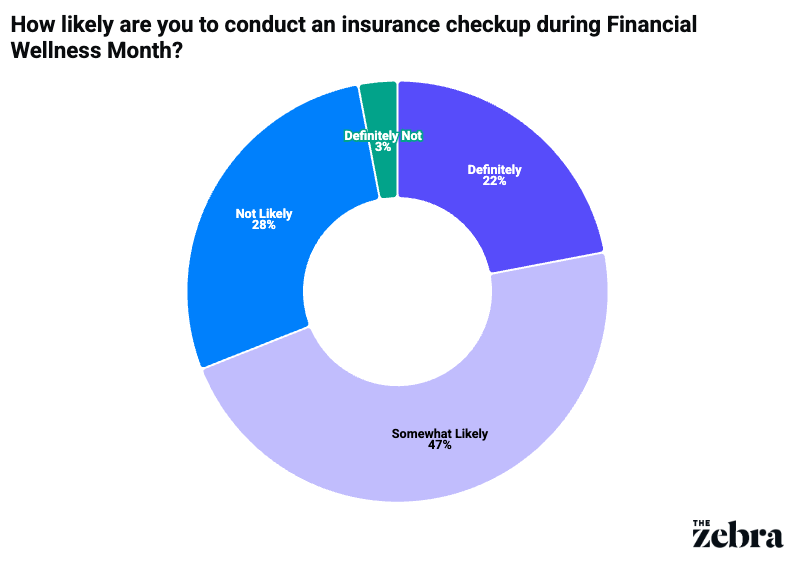

According to a recent national survey by The Zebra, 69% of policyholders are at least somewhat likely to conduct an “insurance checkup” in January to look for savings and improve coverage.

Financial wellness planning involves more than just budgeting or saving. It’s about being prepared for life’s uncertainties and protecting your financial security.

“It also means making sure that insurance risks are properly managed so that unexpected events don’t wreak havoc on your household,” , vice president of Media Relations for the Insurance Information Institute, says.

Worters adds that policies, coverage levels and personal circumstances change over time. That’s why a regular review of your insurance coverages can help you identify potential gaps and confirm that the protection you have in place aligns with your current needs.

The Role of Financial “Shock Absorbers”

From and home damage to theft and claims, there are many financially destabilizing events that put households at risk. Fortunately, you can buffer these threats to your wallet by having safeguards in place — including an emergency fund, performing needed to your home, installing around your property, and having necessary insurance coverage.

“Suffering $50,000 of property damage or a $100,000 liability claim without the right coverage could be catastrophic. Adequate insurance promotes financial health by shifting catastrophic risks to an insurer,” Ferrara says.

Auto, home and renters insurance are designed to protect your income, savings, and long-term financial goals. Think of insurance as a way to trade uncertainty about the unexpected for predictability.

How Homeowners Insurance Supports Financial Wellness

Having solid is a smart way to protect the investment you’ve made in your property as well as your overall financial stability.

“A homeowners policy protects more than just your home’s structure. It typically covers your personal belongings, detached structures like sheds or fences and additional living expenses if you can’t stay in your home after a covered loss,” notes , insurance analyst for The Zebra. “Liability coverage is another critical part of homeowners insurance. If someone is injured on your property, you could be held financially responsible, and those costs can add up quickly, which is where liability coverage comes in handy.”

You want to check that you have sufficient to rebuild your home if it’s severely damaged or destroyed. A good starting point is to learn the average cost per square foot to build a new home in your area and multiply that by your home’s square footage. Then, you can fine-tune other coverage limits based on your needs.

“It’s also important to choose a you can realistically afford. This is the amount you pay out-of-pocket when you file a claim before insurance coverage applies — often deducted from the final payout,” Swanson continues. “While higher deductibles can lower your premium, they only make sense if you have enough emergency savings to comfortably cover that amount if something goes wrong.”

Remember that life changes quickly, and events like moving, , or shifts in income can impact how effective your existing coverage is. Take the time to re-examine your homeowners policy every few months to ensure you have the right protection in place. And if you choose to shop around among different insurers, be sure to compare coverage, not just price.

Auto Insurance and Financial Stability

Having adequate isn’t just strongly recommended by the experts: It’s a legal requirement in every state (except ) that you at least carry liability coverage, which pays for property damage and injuries you are at fault for. Many states also require , or personal injury protection and medical payments.

The Insurance Information Institute recommends having liability protection that covers $300,000 per accident and $50,000 in property damage. Collision and comprehensive coverage is also strongly recommended.

“Your deductible will influence your out-of-pocket exposure. A higher deductible lowers premiums but requires more immediate cash after a claim,” Worters notes. “By balancing deductibles and coverage limits, you can protect yourself from financial shocks while maintaining affordable premiums.”

Renters Insurance as Asset Protection

If you rent instead of owning a home, renters is a wise purchase because it safeguards your belongings and provides liability protection, even though you don’t own the building. It prevents major financial losses in the event of theft, fire or water damage, and can cover legal costs if someone is hurt in your unit.

“It’s also affordable, often costing less than $30 a month, and can prevent major financial losses from theft, fire or water damage from something like a burst pipe. Deductibles of $500 to $1,000 and coverage that reflects replacement cost rather than actual cash value are recommended,” says Worters.

What Financial Wellness Looks Like in Practice

Insurance-related financial wellness means being prepared before something goes wrong, not learning the hard way in the middle of a claim.

“Most people don’t pay much attention to their insurance until they need it. But that’s often one of the most stressful moments for policyholders and not the time to discover coverage gaps or limitations,” Swanson says.

While you don’t need to memorize your entire policy, familiarize yourself with key details on your , especially what your deductible is, what types of losses are and aren’t covered, and if you own a home, how much coverage you’ll need to rebuild it.

“Consumers can improve their financial wellness by approaching insurance proactively,” suggests Worters. “Compare rates and options from multiple insurers for competitive pricing and coverage that meets your needs. Select deductibles and coverage limits that balance affordability and adequate protection. Consult licensed insurance professionals to identify gaps and ensure optimal coverage.”

was produced by and reviewed and distributed by ¬È∂π‘≠¥¥.