Sectors to consider when investing in 2026

Investors who navigated 2025 with diversified portfolios didn’t just reduce risk—they enhanced returns. In 2026, the playbook for many investors remains balanced: Stay invested in large-cap AI leaders while broadening exposure beyond the narrowest part of the market. highlights three aspects of portfolio construction to pay attention to this year.

Maintaining Exposure to AI and Big Tech Without Going All In

Concerns of an AI bubble abound, and they may yet be realized, but that doesn’t mean investors should abandon Big Tech entirely.

The velocity of innovation and growth in the AI sector is simply too high to ignore. The productivity revolution underway is fundamentally reshaping the global economy. Regardless of where valuations stand today, eliminating exposure to large U.S. tech companies at the epicenter of this trend creates a distinct risk for those on the sidelines.

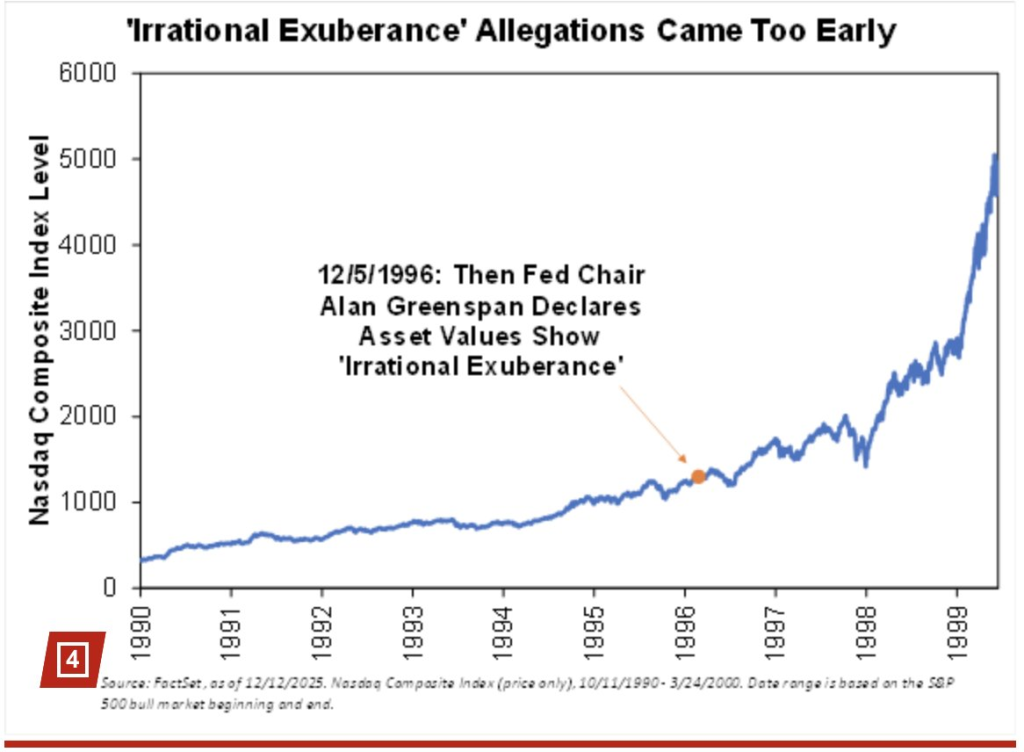

For long-term investors, the opportunity cost of exiting too early is meaningful. Consider the “Dot-Com” era. An investor who sold tech stocks in 1997 because they looked “expensive” missed the structural gains of the following three years. Even after the crash of 2000, the investor who held through the cycle often ended up ahead of the investor who exited prematurely.

This is particularly relevant in 2026. Unlike the dot-com peak—when the Fed was hiking rates and the regulatory environment was uncertain—today’s AI boom is occurring against the backdrop of a supportive Fed and increasing fiscal stimulus. Betting against a technological revolution is difficult enough; betting against one that is backed by could be even riskier.

Small and Midcap Stocks Could Offer Exposure to a Different Part of the Economic Cycle

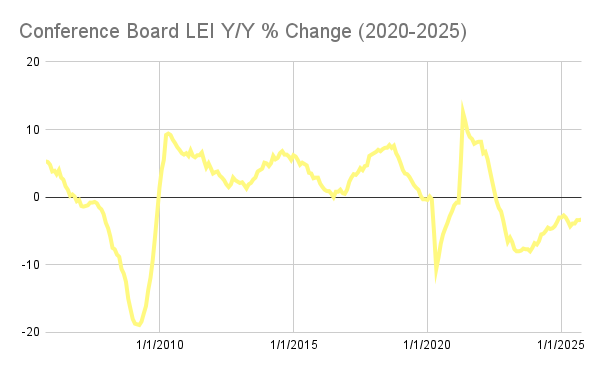

Despite strong headline market performance, large parts of the U.S. economy have been in a rolling slowdown for years—and are only now starting to turn. Manufacturing spent much of the past three years in contraction: The was below 50 for 26 consecutive months before returning to expansion in early 2025. Meanwhile, the Conference Board’s has remained persistently weak since mid-2022—at one point logging 23 straight monthly declines—an unusually long warning streak without an official recession.

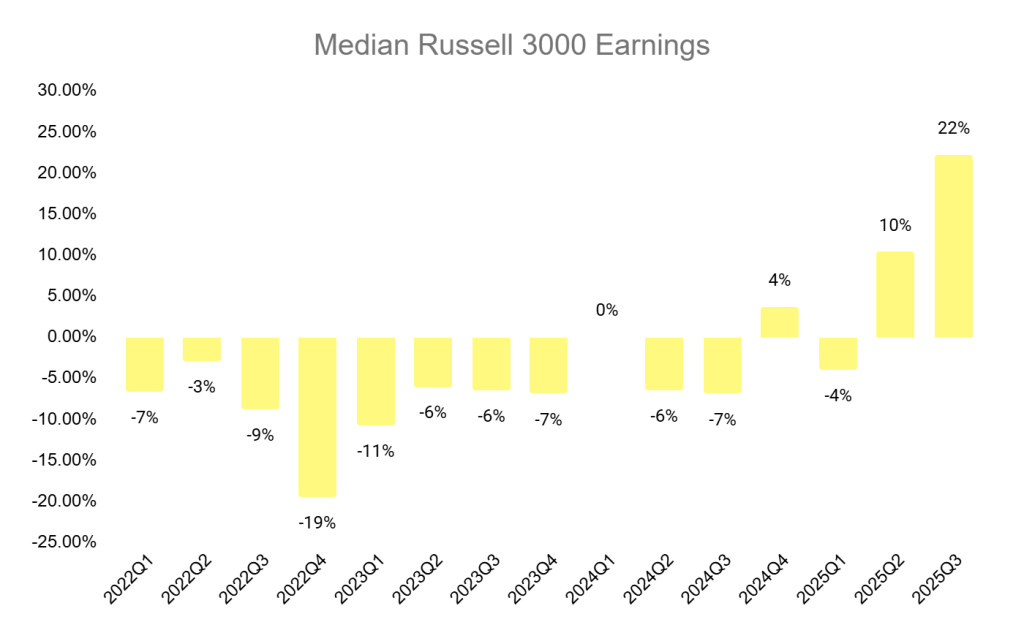

This malaise shows up when you look beyond headline index earnings. While S&P 500 profits have been disproportionately supported by the “Mag 7,” earnings for the typical U.S. company have been far more subdued and only recently improving. The median stock in the Russell 3000—an index that represents roughly 98% of the investable U.S. equity market—has seen lackluster earnings momentum in recent years and is only now beginning to inflect.

Many of these companies are AI beneficiaries—not as hyperscalers, but as adopters integrating AI to boost productivity:

“In terms of the language courses, we added 148 new language courses. All of this content was done with AI, and it really took us about a year to add these 148 language courses. And like you mentioned, the previous 100-ish courses took us about 12 years to make. So this is an incredible speed-up.” – Duolingo Q1 2025 Earnings Call

“And so we probably didn’t get as much press on this, but in the last quarter…[we saw] through automation and through AI, a 61% improvement in productivity year-over-year. And [we] don’t have less brokers — we’ve redeployed them in other places to generate freight” – Schneider International at MS Industrials Conference in Q3 2025

“Our margins expanded by 90 basis points sequentially as sizable automated startups and productivity initiatives... matured more quickly than expected.” – RXO Q2 2025 Earnings Call

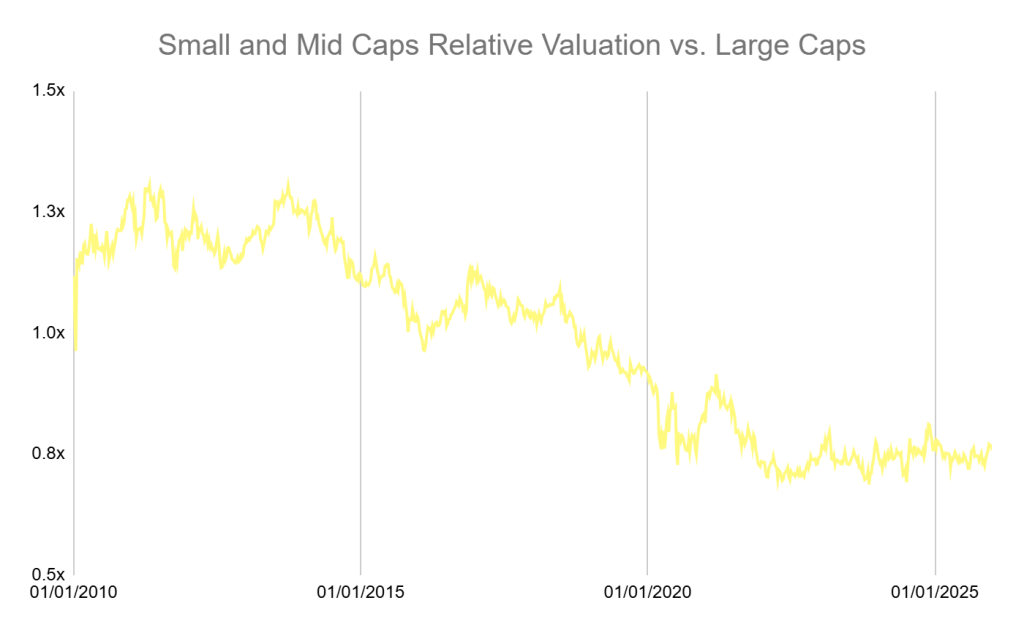

Despite improving earnings trends and increasing evidence of AI-driven productivity, small and midcap stocks continue to trade at a historically wide discount to large caps. If earnings revisions keep trending higher, this segment of the market stands to benefit from a powerful combination: accelerating earnings growth combined with valuation multiple expansion. When this dynamic last occurred between 2020 and 2021, small and midcap stocks outperformed the S&P 500 by over 20%.

International Stocks Can Provide Uncorrelated Opportunities

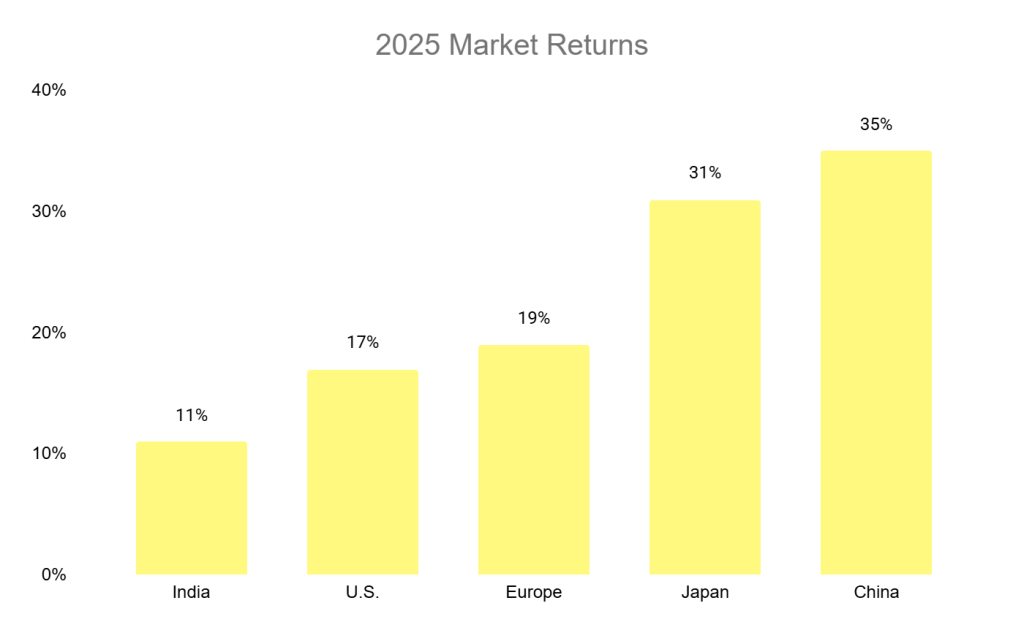

After years of U.S. dominance, 2025 proved domestic outperformance isn’t guaranteed. International equities outpaced the S&P 500, helped by a weaker dollar and a catch-up in valuations outside the U.S.

Heading into 2026, the rest of the world has credible, region-specific tailwinds that can sustain continued performance, especially from a starting point of generally lower valuations.

Europe

- Fiscal pivot (Germany): Germany’s shift from historic restraint to a large, multi-year investment push—via a 500 billion euro infrastructure fund and broader fiscal flexibility—changes the region’s growth mix and supports cyclicals.

- Rearmament and industrial demand: NATO allies committed to a path toward higher defense-related spending (including a stated 3.5% “core defense” goal by 2035), which is a structural tailwind for defense, aerospace, and parts of European industrials.

- AI as a margin story: Europe’s market composition skews more toward “old economy” sectors, including industrials, materials, and financials—where AI adoption can show up as efficiency and margin expansion, not just “AI revenue.”

China

- The “Other” AI Powerhouse: China is explicitly pursuing AI self-reliance—across chips, models, and deployment—supported by policy and state-linked capital, even as U.S. export controls remain a constraint.

- Valuation: Its tech giants—the “Mag 7 of the East”—are growing earnings but trade at historic discounts (8-10 times P/E) versus their U.S. peers. This offers exposure to AI growth without the valuation premium.

India

- Best-In-Class Growth: India remains one of the fastest-growing major economies, with the IMF projecting around a 6.4% growth in both 2025 and 2026.

- Favorable Demographics: A large, young workforce and rapid digitization continue to support domestic demand and formalization—tailwinds that are less tied to the global cycle.

International markets offer more than just a valuation discount; they can offer a different way to win. By allocating globally, investors can own some of the “picks and shovels” of the hardware supply chain and access distinct macro catalysts that provide return drivers uncorrelated to the U.S. tech sector.

Playbook for 2026

2026 can be a year where market leadership broadens.

1. Maintaining Core Exposure to AI Leaders: Despite elevated valuations, the large-cap U.S. stocks remain the primary engines of global earnings growth. We are in the midst of a capital expenditure super-cycle that rivals the build-out of the internet. Exiting a generational technological shift early can be more costly than riding out volatility. These best-in-class companies can be the foundation of a growth portfolio.

2. Capturing the “Real Economy” Rebound (Small and Midcap): Small and midcap stocks offer a dual benefit: a hedge against mega-cap concentration and an offensive play on the U.S. economic recovery with high operating leverage—essentially buying the “real economy” at a historic discount.

3. Participating Globally: International markets offer more than just a value play; they offer distinct drivers of return that are uncorrelated to the U.S. consumer. Distinct local catalysts—such as Germany’s fiscal pivot or India’s demographic boom—provide growth engines that can deliver even if the U.S. slows. International allocations also allow investors to own broad AI exposure at a meaningful discount to U.S. multiples.

Diversification in 2026 is not just about playing defense; it is about capturing the rest of the recovery. By rebalancing into these lagging sectors while holding winners, investors can mitigate the risks of an AI sentiment shift while exposing their portfolios to the parts of the market with the most room to rerate.

was produced by and reviewed and distributed by Â鶹Դ´.