Here's why millions of Americans are unable to sell their homes

If youŌĆÖve typed ŌĆ£canŌĆÖt sell my houseŌĆØ into a search bar recently, youŌĆÖre in enormous company ŌĆö and thatŌĆÖs not a coincidence. It reflects something very real: a housing market that has quietly frozen in place, even as spring brings fresh ŌĆ£For SaleŌĆØ signs to every neighborhood.

This situation isnŌĆÖt about your house, paint colors or even your yard. ItŌĆÖs years of economic forces colliding at once, leaving millions of ordinary homeowners feeling trapped in the very homes they worked so hard to own.

paints the full, honest picture.

Why are so many people searching ŌĆścanŌĆÖt sell my houseŌĆÖ right now?

The spike in searches tells a story before even getting to the statistics. This isnŌĆÖt 2008, when prices collapsed and buyers vanished. TodayŌĆÖs market is more maddening: Home prices are still historically high, but buyers are hesitant, homes are sitting longer and sellers are being forced into painful choices.

According to , the typical U.S. home that sold in March 2026 spent 63 days on the market ŌĆö the longest stretch in six years, and roughly a week longer than a year ago. Pending home sales fell 1.3% year over year. The market is stalling, not collapsing, but for a homeowner who needs to move, that distinction can feel meaningless.

The invisible force freezing the market

To understand why selling is hard right now, you need to understand the mortgage rate lock-in effect ŌĆö arguably the most powerful force in American real estate today.

During the COVID-19 pandemic, the Fed slashed rates to near zero. Millions locked in at rates as low as 2.65%. Moving now means giving up that rate forever and stepping into a new rate in the low-to-mid 6% range. On a $400,000 loan, thatŌĆÖs roughly $700 more per month ŌĆö over $8,000 a year.

A February 2026 survey by Storable found that 73% of homeowners would consider moving if they could transfer their current rate. One in 4 with rates below 5% said no amount of money would convince them to give it up. Academic research estimates the lock-in effect reduced nationwide home sales by more than a million transactions and inflated prices 5% to 6% above where theyŌĆÖd otherwise be.

The good news: According to The Washington Post, the market recently crossed a meaningful threshold. There are now more Americans with mortgage rates above 6% than below 3%. The lock-in effect is loosening ŌĆö just not fast enough for the homeowner staring at a listing that wonŌĆÖt move.

Your neighborŌĆÖs 3% rate is your problem too

HereŌĆÖs something nobody talks about enough: Your neighborŌĆÖs rock-bottom might be good for them, but itŌĆÖs actively hurting your sale.

When the family next door locked in 2.9% in 2021, they may have had every intention of eventually . Then rates doubled. Now theyŌĆÖre staying put, their home isnŌĆÖt coming to market, and the buyers in your area have fewer options to choose from ŌĆö which sounds like it should help you, but hereŌĆÖs the twist: Those same buyers are also stretched thin by high prices and high rates affecting whether they . TheyŌĆÖre cautious. TheyŌĆÖre negotiating hard. TheyŌĆÖre walking away from anything that feels overpriced.

YouŌĆÖre caught in the middle: not enough seller competition to feel scarce, not enough buyer confidence to feel urgent. ItŌĆÖs the worst of both worlds, and itŌĆÖs playing out in living rooms across the country right now.

What the numbers actually say

HereŌĆÖs where things stand, from the most trusted sources in housing:

Mortgage rates (March 2026)

reported the 30-year fixed rate at 6.11% as of March 12, 2026, with rates hitting 5.98% on Feb. 26, 2026 ŌĆö the first time in 3.5 years it dipped below 6%. A year ago, it averaged 6.65%. are improving but remain a universe away from the 2.65% low of January 2021.

Home prices

The National Association of Realtors (NAR) reported a median existing-home sales price of $398,000 in February 2026. National forecasts project 1% to 4% price growth for the year, with the Midwest and Northeast seeing stronger gains and parts of the South and West going flat.

Inventory

The NAR reported 3.8 months of supply, still below the four to six months considered a balanced market. Critically, much of the inventory growth isnŌĆÖt from new sellers listing homes. ItŌĆÖs from homes sitting on the market longer.

Sales volume

Existing-home sales decreased 1.4% year over year in February 2026, data. NAR Chief Economist Lawrence Yun noted: ŌĆ£Housing affordability is improving, and consumers are responding. ŌĆ” Still, there is a long way to go to return to pre-pandemic levels of transaction activity.ŌĆØ

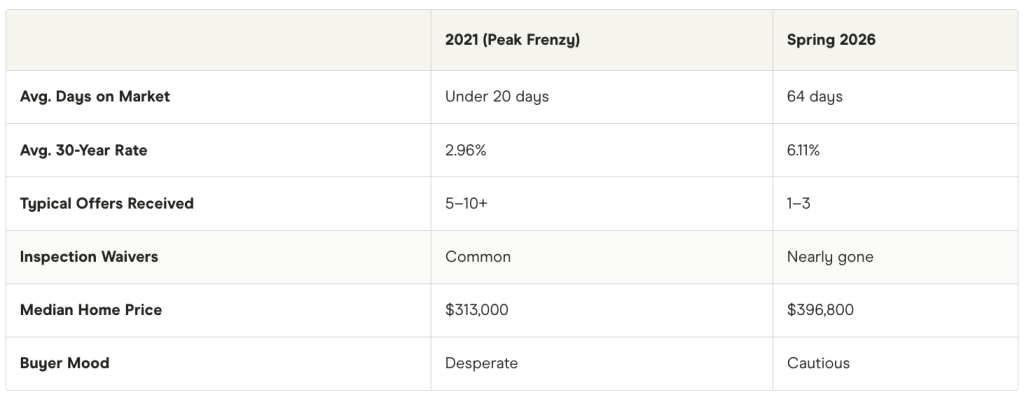

Selling a house in 2026 vs. 2021: A tale of two markets

Sometimes the best way to understand where you are is to see where youŌĆÖve been. Consider this:

The homes that sold in 2021 practically sold themselves. In spring 2026, sellers have to earn the sale with smart pricing, strong presentation and patience.

Why buyers arenŌĆÖt jumping either

Even with rates dipping below 6% for the first time in years, buyers are hesitant. RedfinŌĆÖs 2026 housing mood report describes them as taking their time, requesting inspections and negotiating ŌĆö behaviors almost unheard of during the pandemic frenzy.

The core reasons: Median home prices have risen roughly 25% since 2019, per U.S. Census data. Monthly payments on a median-priced home still run around $1,922 ŌĆö about 22% of the typical familyŌĆÖs monthly income.

And StorableŌĆÖs survey found that 38% of would-be buyers say they need rates below 4.5% before theyŌĆÖd seriously consider buying. With rates in the mid-6% range, more than half of potential movers are waiting for a rate drop that most economists say isnŌĆÖt coming anytime soon.

What you can actually do

- Price for the market that exists, not 2022. Overpricing is the single biggest reason homes sit. Delistings ŌĆö sellers pulling listings rather than accepting lower offers ŌĆö rose to 32% of new listings in January 2026, up from just 8% in January 2022, per Realtor.com. Sellers who start wrong almost always end up lower than they would have if theyŌĆÖd started right.

- Make it move-in ready. Buyers in 2026 are flagging repairs and walking away from homes that need work. A focused spend on cosmetic updates, such as paint, landscaping and minor fixes, can dramatically shift buyer perception.

- Explore your financing options. Bridge loans, , , or even can give you the financial flexibility to make your next move without being held hostage by your timeline. If rates continue easing, the math on some of these tools is getting more attractive by the month.

- Know your window. Spring and early summer historically remain the strongest listing seasons. And with rates now under 6% and the NAR projecting existing-home sales could rise as much as 14% in 2026, the buyer pool is growing slowly.

A final word: This is not your fault

The 2026 housing freeze is the result of a decade of underbuilding, two years of emergency monetary policy, three years of rate shock and a pandemic that reshuffled where Americans want to live ŌĆö all colliding at once.

But the freeze is thawing. . Inventory is improving. Affordability, per NARŌĆÖs own index, just hit its best level since March 2022. These are real signals.

If you need to move now, you donŌĆÖt have to wait for a perfect market. You need the right strategy for the market that exists. And if is part of that strategy, knowing your options is the most powerful first step you can take.

was produced by and reviewed and distributed by ┬ķČ╣įŁ┤┤.