How to spot a mortgage scam in 2025

If there’s one thing you should know going into the home-buying or refinancing market this year, it’s this: Mortgage scams are evolving faster than ever. From phishing tactics to impersonation of lenders and fake “mortgage relief” firms, scammers are exploiting economic stress, interest rate volatility, and fears around housing instability.

- According to an industry report by , the National Mortgage Application Fraud Risk Index jumped 6.1% year-over-year in 2025.

- Some industry commentary notes that monthly mortgage scam reports have increased over 400% since 2022 (from 14 to 71 per month), though only about 12% of those reported included a confirmed loss, according to BackOfficePro’s report.

- The to homeowners who paid sham mortgage relief companies that never delivered promised services.

In short: The cost to victims can be massive — lost equity, ruined credit, even foreclosure. And the regulatory agencies are actively warning of new methods and red flags. highlights what you need to know now, and why the FTC is sounding the alarm.

What the FTC and Regulators Are Saying (2025 Alerts and Wisdom)

The FTC has long flagged mortgage relief scams (where a company claims it can negotiate a better deal on your mortgage for an upfront fee) as a frequent fraud vector.

Recent Remediation and Pushbacks

- In January 2025, the FTC sent refunds to consumers who paid into a sham mortgage relief operation, HOPE Services and HouseHoldRelief, that didn’t deliver on modifications.

- The FTC is also issuing second-round payments to and related entities that falsely promised mortgage loan relief in exchange for upfront fees.

- Meanwhile, state and federal regulators coordinated to take down a multimillion-dollar mortgage assistance scam targeting distressed homeowners.

These enforcement actions underscore a key rule: It’s illegal for a company to demand upfront payment before delivering a loan modification or relief.

New Red Flags in 2025

- Fannie Mae updated its “Potential Red Flags for Mortgage Fraud and Other Suspicious Activity” guidance effective April 1, 2025, expanding the set of suspicious indicators lenders should monitor.

- The Federal Communications Commission (FCC) has also — callers claiming to offer mortgage relief or assistance via spoofed numbers to appear local or from legitimate lenders.

Regulators are clearly raising the bar on what to watch out for. Below is an updated scam-prevention checklist for 2025.

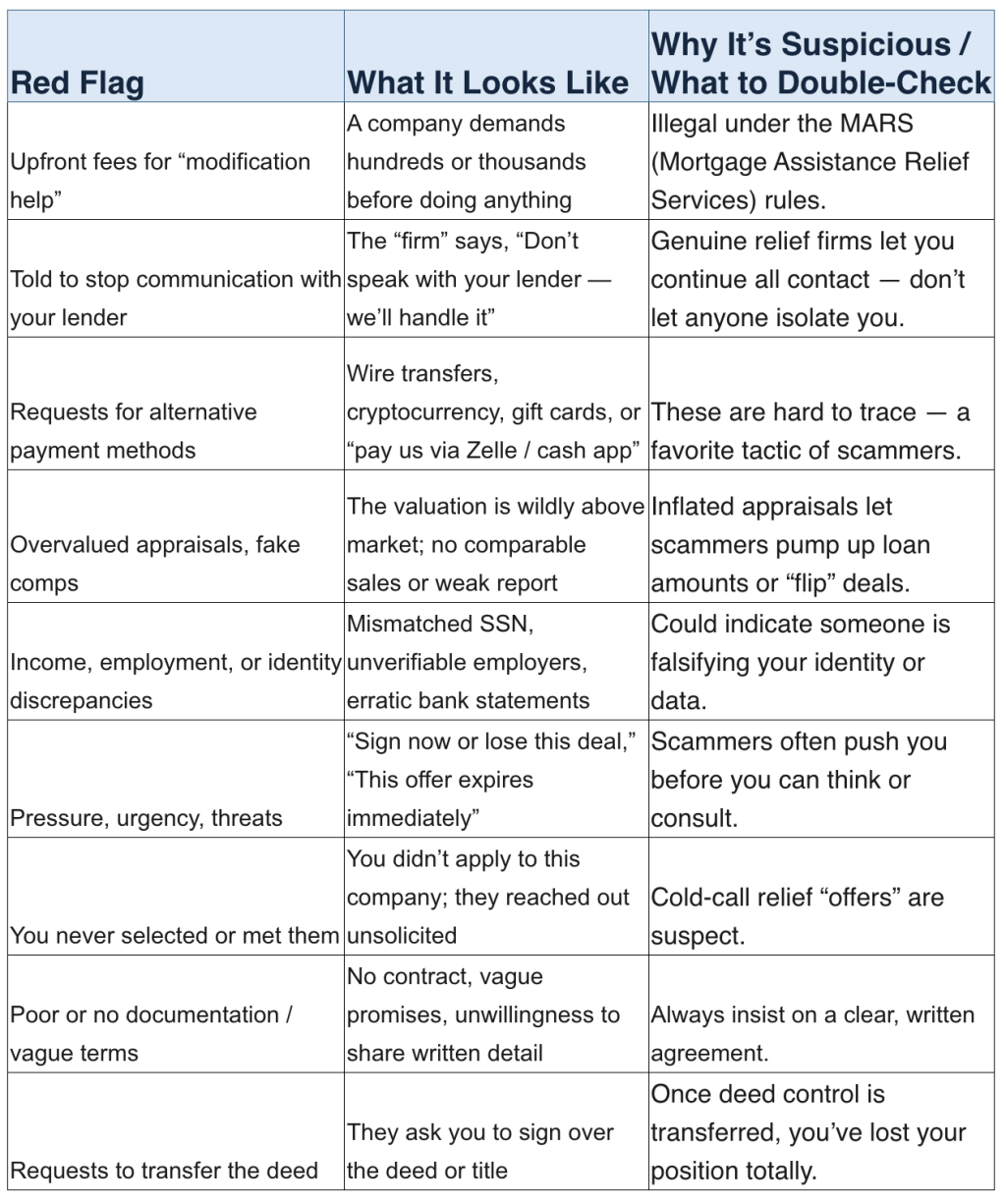

Red Flags: How to Spot a Mortgage Scam Today

Any one of these could be benign — but several together, or a strong gut feeling, should put you on guard.

Note: Some red flags come from internal lender audits, too — in 2025, examiners are trained to notice white-outs, squeezed signatures, inconsistent file entries, or missing verification.

Real-World Scam Examples: 2025 Cases to Learn From

1. Sham Relief / Upfront Fee Operation (HOPE / HouseHoldRelief)

A firm claimed to be a nonprofit with government ties; homeowners were told to pay before any relief actions, and in many cases nothing ever got passed on to the lender. The FTC is refunding payments to victims.

2. Consumer Defense and Related Entities

They used names like “Preferred Law,” “American Home Loans,” and “Modification Review Board,” promising to reduce payments. Instead, they led homeowners to stop paying the lender, told them not to talk to anyone else, and pocketed the funds. The FTC issued refunds and bans.

3. “Green Mirage” Spoof Calls

Scammers call using spoofed phone numbers that mimic your lender or a known mortgage servicer, offering “assistance” to lower your payment. They ask for your account details or money. This trick is gaining traction in 2025.

4. Title / Deed Transfer Scams

In desperate scenarios, facing foreclosure to “sell” or assign the deed to the scammer with promises of “buy-back” or relief. Once deed control is theirs, the homeowner is powerless.

What You Can Do: Smart Practices to Stay Safe

Here are proactive steps to protect yourself.

Always independently verify

- Use your lender’s known phone number (not one given by a third party).

- Check state bar associations if someone claims to be a lawyer.

- Look up complaint histories or reviews.

Demand fully written agreements

No handshake deals. No “we’ll send later.” Insist on clear terms, obligations, and timelines in written contracts.

Never pay upfront for mortgage relief

This remains a red line rule in FTC guidance.

Maintain communication with your lender

Don’t be dissuaded from discussing options directly with your mortgage servicer or a Department of Housing and Urban Development-approved housing counselor.

Monitor your credit and property records

- Use credit monitoring alerts.

- Check your county’s property records for unauthorized filings or transfers.

Pause if pressure feels extreme

A legitimate provider will respect your need to review, consult, and think — not push you over a decision in minutes.

Report suspicious activity immediately

- File a complaint at ReportFraud.ftc.gov.

- Contact your state attorney general’s consumer division.

- Inform your lender, and local real estate or bar associations when applicable.

A Snapshot: Mortgage Scam Trends and Projections

While real-time comprehensive data for 2025 is still emerging, we can look at what’s known so far.

- Mortgage fraud risk indices are rising — BackOfficePro’s report shows a 6.1% year-over-year increase was reported in 2025, according to BackOfficePro.

- Scam volume is climbing — the same report tracking mortgage scam reports observed a 407% increase since 2022.

- Regulators are pushing back — the FTC has refunded victims in multiple mortgage relief fraud cases in 2025.

Final Thought: Don’t Be the Next Victim

Homeownership marks one of life’s most important financial steps, but it also invites scrutiny from bad actors. In 2025, with more automated tools, identity theft, voice spoofing, and remote closing processes, scammers have more levers than ever.

Stay skeptical, stay informed, and consult trusted professionals (realtors, attorneys, housing counselors) when something doesn’t feel right. The FTC and other regulators are watching, but the best line of defense starts with you.

was produced by and reviewed and distributed by Â鶹Դ´.