Why car prices are so high today

Has it been a while since youāve walked into a new vehicle showroom? Expect some serious sticker shock. The typical MSRP for a new ride nowadays is halfway to six figures. Considering steeper purchase prices, itās little wonder that many drivers or opt for used cars.

Whatās behind these costly new vehicle prices? Alternatively, what can you expect to pay for a used auto today? What are some factors you need to consider carefully before committing to a vehicle purchase? And how can you shave serious dollars off your car transaction? shares answers to these and other questions.

How Much Does It Cost to Own a Car in 2026?

The average transaction price for a new vehicle is currently $49,814, up 1.3% from one year ago, according to November 2025 (KBB).

Of course, out-the-door dealership price isnāt the only expense drivers need to take into consideration. On average, owning and operating a , according to AAA.

Hereās some of how that breaks down:

- The average consumer spends around every year, WalletHub reports.

- Additionally, Americans now fork over an , according to recent data from KBB.

- The in the United States is currently around $2,256, based on The Zebra data.

- Also, consider that, according to a recent study by doxoINSIGHTS, with these bills adding up to 9% of total consumer household bills per year. The median monthly auto loan bill is $470, totaling $5,640 annually.

āBeyond the sticker price, buyers need to budget for sales tax, title and registration fees as well as dealer/documentation fees,ā says automotive industry expert Lauren Fix, author of Car Coach Reports. āOn a typical new vehicle, fees and insurance plus some upfront costs can easily add up to an additional $2,000 upfront.ā

Why New Car Prices Were So High in 2025

So, why do vehicle prices remain so elevated? The reasons are plentiful, the experts agree.

āIn 2025, new on imported cars and auto parts increased manufacturersā costs, leading to higher prices for buyers. One analysis estimates these tariffs could raise car prices by 10%, or add about $5,000 to the average price of a new car,ā says , an insurance analyst at The Zebra. āAt the same time, the cost of materials and key components ā including computer chips ā has gone up, and ongoing supply chain delays continue to slow production and add expense.ā

Rami Sneineh, vice president at Insurance Navy Brokers, points out that the semiconductor shortage during the pandemic severely hampered the production of new vehicles, making a recovery difficult.

āEven when factory capacity returned, the skyrocketing costs of labor and materials helped raise sticker prices even higher than they were in the pre-pandemic era,ā Sneineh explains.

Mandated technology, high interest rates and demand for larger and more advanced vehicles have also contributed to steeper new car prices.

āThere is an increased tendency toward bigger cars like SUVs and trucks, which are inclined to be more expensive than smaller cars, raising the average cost of purchases,ā Sneineh continues.

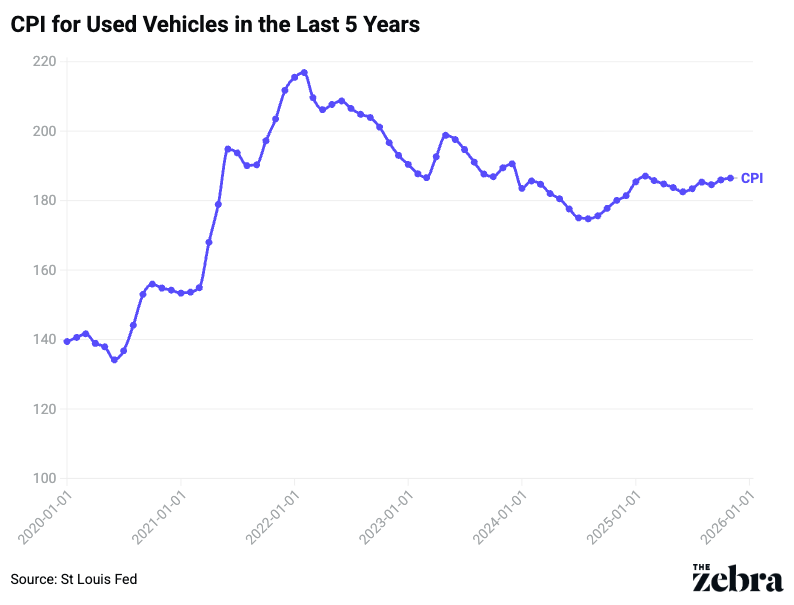

How Used Car Prices Have Changed

Eager to save money on a pre-owned set of wheels? KBB indicates that the average used car right now has a .

If youāre in the market for a used vehicle below $15,000, itās slim pickings: Dealerships only had around a 34-day supply in late 2025, which is two weeks below the industryās overall average. Additionally, potential tariff price pressures could worsen matters; many consumers look more closely at the used market when new autos become more costly, which further dilutes already sparse used inventory.

Ponder, as well, that many drivers retain their cars for longer, with the average vehicle on the road now . Consequently, the most attainable used car now typically falls in the $15,000 to $30,000 range.

āPrices continue to rise, with 1- to 5-year-old used vehicles now averaging about $31,770 ā up nearly 4% from last year,ā Fix continues. āOverall, the market is still far more expensive than pre-2021 levels, and the gap between new and used prices remains unusually small.ā

What Car Buyers Need to Think About

Itās smart to be well prepared before heading to a dealership or meeting with a used car seller. That means:

- Determining your budget and .

- Thinking carefully about the type of car you want to purchase and how long you plan to own it.

- And learning if your credit is worthy enough to qualify for a better rate and terms if you need financing.

āHigh car prices combined with higher interest rates mean youāll likely face larger monthly payments. With an average new car loan rate around 7% today, and a typical term close to 69 months, affordability is often stretched thin,ā says Fix, who adds that financing a $50,000 car at 7% over 60 months will result in a car loan payment of around $1,000 per month ā before adding insurance, taxes, and fees.

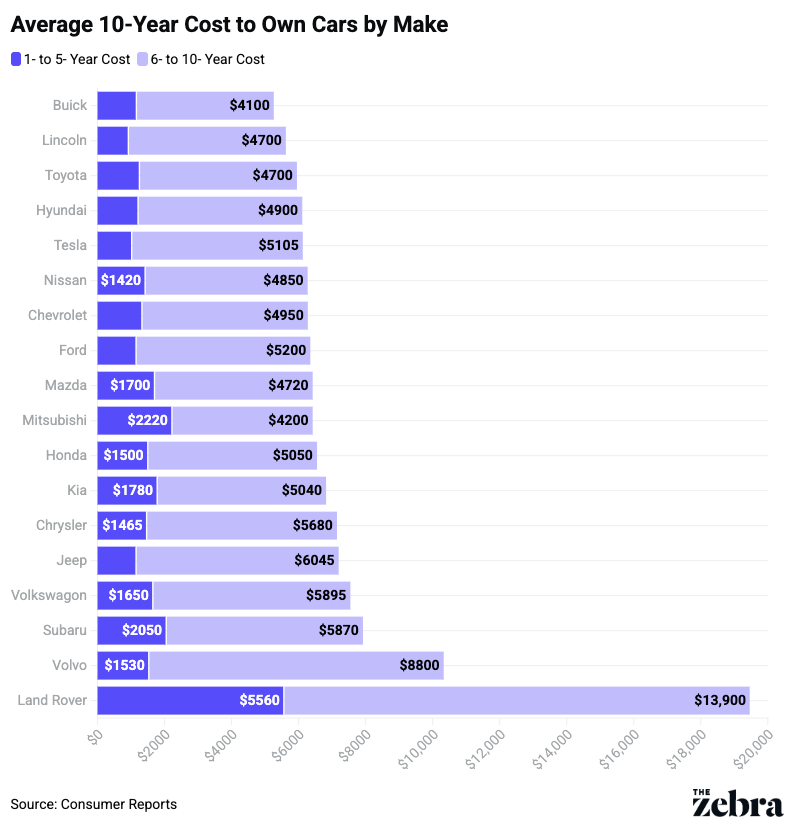

Additionally, ponder long-term fix and upkeep expenses based on your desired make and model. Per a of lowest repair and maintenance costs by brand, Tesla tops the list with approximately $4,035 in total 10-year maintenance expenses, followed by Buick and Toyota at about $4,900 each, and Lincoln at around $5,040. Mainstream mass-market brands like Ford, Chevrolet, Hyundai, Nissan, Mazda, and Honda also fall on the lower-cost end. In contrast, European luxury vehicles tend to be the most expensive: Land Rover can surpass $19,000 over 10 years, Porsche around $14,090, and Mercedes-Benz about $10,525.

āRemember, too, that the type of vehicle you choose affects your insurance costs,ā Swanson adds. āOlder, reliable and safe cars usually cost less to insure than newer luxury models or high-performance sports cars. But only part of your insurance rate is based on the vehicle itself. Your matter even more ā things like your age, driving history and where you live play a major role in what you will ultimately pay for car insurance.ā

Tips for saving money on a car purchase

Want to spend less on a new or used car? These expert-backed strategies can help cut costs.

- Shop beyond your zip code. Prices can vary widely by location, so expanding your search may unlock better deals.

- Time your purchase carefully. āDealers are far more motivated to bargain in the last week of any month or quarter,ā says Fix.

- Ask about incentives. Look for manufacturer rebates, special financing, or loyalty discounts.

- Avoid expensive extras. āOptional dealer add-ons, especially cosmetic packages and extended warranties, can be extremely expensive,ā warns Sneineh.

- Buy slightly used. āThe sweet spot is a 3-year-old car, preferably a former lease,ā says personal finance expert Paul Walker.

- Check the vehicle history. A low-cost report can reveal prior accidents or serious damage.

- Size and trim matter. Choosing a smaller vehicle or mid-level trim can lower both purchase price and ownership costs.

- Get preapproved financing. Credit unions and online lenders often offer better rates than dealer financing.

- Avoid long loan terms. Shorter loans usually cost more per month but reduce total interest paid.

- Do the math on EVs. Higher upfront and insurance costs may offset fuel savings.

- Consider certified pre-owned or off-lease vehicles. These options can significantly reduce monthly payments with minimal compromise.

- Negotiate the out-the-door price. Focus on the total cost, including taxes and fees, not just the monthly payment.

- Be ready to walk away. If the deal doesnāt feel right, leaving may be your strongest leverage.

was produced by and reviewed and distributed by Ā鶹Ō““.