How to invest your tax refund in 2026

The average American is getting a $3,521 tax refund as of March 27, 2026, according to the IRS ŌĆö thatŌĆÖs over 11% more than the average 2025 refund. The One Big Beautiful Bill Act gave Americans new tax breaks, including eliminating most income tax on tips and overtime, allowing a deduction for certain auto loan interest, and creating a new deduction specifically for seniors. As a result, tax refunds are higher than ever.

If youŌĆÖre set to receive a big tax refund, one of the smartest moves you can make is to use the money to set yourself up for a by investing some or all of the money you get back, reports.

This article dives into some of the best ways to put your tax refund to work, including suggestions from The Motley FoolŌĆÖs financial planning and investing experts.

Key Points

- Average American tax refund rises to $3,521 as of March 27, 2026, an 11% increase from 2025.

- Best uses of tax refunds include clearing high-interest debt and building emergency funds.

- Investing in the stock market, especially index funds, is generally advised for long-term wealth growth.

4 of the best ways to invest your tax refund

When it comes to investing your tax refund, there are literally hundreds or even thousands of ways you can choose to do it. But the best options can be divided into four main categories.

1. Pay off high-interest debt

This one might not seem like an "investment," but consider: Over the long term, the stock market produces returns of 9%-10% per year, on average. While not guaranteed in any given year, some of the best investors can consistently manage returns in the 12%-14% ballpark. So, if you invest in stocks, mutual funds, or ETFs while you have credit card debt at 21% interest, youŌĆÖre setting yourself up to lose money over time.

If you have high-interest debt, which can be loosely defined as anything with a double-digit interest rate, it can be a wise idea to pay it off before you think about investing money elsewhere. The average American has about $6,500 in credit card debt, so many people can benefit from this. The good news is that the average tax refund would cover more than half of this amount.

2. Build your emergency fund

HereŌĆÖs another one that might not seem like an ŌĆ£investmentŌĆØ at first. But letŌĆÖs say you invest your tax refund in stocks, then your car gets a flat tire, and you have no savings. YouŌĆÖd be forced to sell the investments you just bought ŌĆö or worse, put the expense on a high-interest credit card.

Most financial planners recommend that you aim to have six monthsŌĆÖ worth of expenses in an easily accessible place, like a . This might sound like an intimidating amount of money, but you donŌĆÖt need to get there right away. Even a $1,000 emergency fund will put you in a position to handle most unexpected expenses, and youŌĆÖll be in a better position than many Americans.

3. Invest in the stock market

Now for the fun part. Investing in the stock market over the long term is the most surefire way to build wealth. But that doesnŌĆÖt mean that you need to invest in individual stocks (although if you have the desire, it can be a great way to go).

One way to get exposure to the stock market is through , which are low-cost investment vehicles that give you exposure to an entire group of stocks ŌĆö such as the S&P 500 ŌĆö in a single investment.

In an interview with USA Today, Robert Brokamp, CFP, senior advisor and financial planning expert at The Motley Fool, said, ŌĆ£I think everyoneŌĆÖs retirement should be built on a foundation of index funds. And then you can gradually move into individual stocks.ŌĆØ

Of course, if you have the time, knowledge, and desire to invest in individual stocks, it can be a great way to go. Here are some suggestions from a few of The Motley FoolŌĆÖs stock analysts:

Get exposure to high-growth industries

Aerospace and defense

ItŌĆÖs no secret that aerospace and defense have been in the headlines quite a bit recently, both because of the Iran conflict and the recent Artemis 2 launch. , a contributing Motley Fool aerospace and defense analyst, says he would split up his refund check between a couple of different investments to broaden his exposure to the :

ŌĆ£IŌĆÖd split my investment between a slow-and-steady winner like TransDigm Group and a higher-risk, higher-reward newcomer like Kratos Defense & Security Solutions. Those two combine to cover some of the hottest themes in aerospace in 2026: The need to restock, and the push by the Pentagon towards more uncrewed and electronics-focused platforms in the years to come."

Energy

Amid volatility in oil and gas markets, Motley Fool energy market analyst highlights an alternative energy company with long-term potential and a strong market position.

ŌĆ£Bloom Energy has a clear path forward for lots of growth. The fuel cell designer and manufacturer continues to see demand rise within the data center markets as traditional power generation from gas turbines remains supply-constrained.ŌĆØ

The best way to invest in electric vehicles?

ThereŌĆÖs more to the electric vehicle industry than companies like Tesla. , a senior contributing Motley Fool auto analyst and former CNBC reporter covering the future of autos, says:

ŌĆ£Like most auto analysts, I believe most vehicles will be electric ŌĆö eventually. But ŌĆśeventuallyŌĆÖ could be a while. Given that, rather than an electric-vehicle start-up, I like General Motors stock right now. This isnŌĆÖt your dadŌĆÖs GM: CEO Mary Barra has GM ready to surge production of EVs on short notice, while making good profits on gas-powered trucks and SUVs in the meantime. GM stock surged in 2025, but I think it still has more room to run ŌĆö and youŌĆÖll collect a decent dividend along the way.ŌĆØ

Set up an income stream

Finally, if youŌĆÖre looking to build a passive income stream ŌĆö for retirement or otherwise ŌĆö Senior Motley Fool investment analyst suggests investing in .

ŌĆ£With that refund, IŌĆÖd strongly consider a small basket of dividend-paying stocks, or a low-cost dividend-focused fund with a great track record like the ,ŌĆØ he said.

ŌĆ£ItŌĆÖs not just about income,ŌĆØ Argersinger adds. ŌĆ£According to several long-term studies of the stock market, including those by Hartford Funds, Ned Davis Research, and OŌĆÖShaughnessy Asset Management, stocks that pay above-average dividend yields or grow their dividends by above-average rates have been the best-performing stocks in the long run with less volatility.ŌĆØ

Also consider adding some high-quality real estate investment trusts (REITs) to your portfolio. Thanks to persistently elevated interest rates, there are some excellent valuations and dividend yields available in the real estate sector. Rock-solid REIT Realty Income has a 5.3% dividend yield and a 30-year track record of consistent dividend increases, and data center REIT Digital Realty Trust has a 2.7% yield and could be a great income play on the boom in AI infrastructure.

These are just a few different examples of in the stock market, but hopefully these can be a nice starting point.

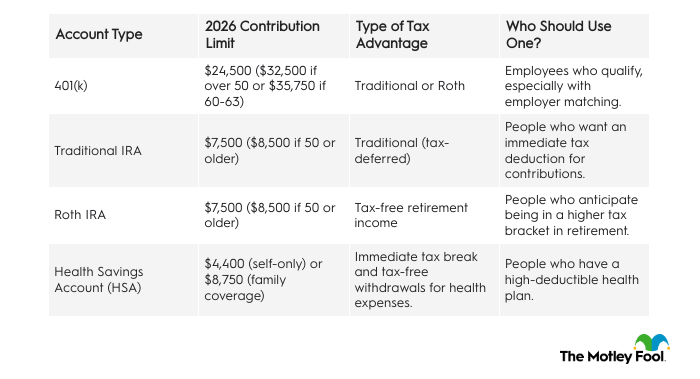

4. Max out tax-advantaged accounts

When you invest in the stock market with any of the funds or stocks discussed in the previous section, there are two main ways to do it. You can contribute money to a taxable (standard) brokerage account, or you can contribute to a tax-advantaged account, which can help optimize your long-term wealth-building potential.

Of course, there are some great reasons to use taxable brokerage accounts ŌĆö for example, you can sell stocks and withdraw money whenever you want. But tax-advantaged accounts allow your investments to grow and compound, with no taxes on dividends or capital gains each year.

Why investing tax refunds makes sense

As mentioned earlier, the average AmericanŌĆÖs tax refund is $3,521 as of March 27, 2026. But if you invest this money, instead of spending it, it could be worth far more to you over the long run. Consider that this amount of money invested at the S&P 500ŌĆÖs average long-term rate of return would be worth roughly $61,500 after 30 years. ThatŌĆÖs why investing your tax refund could be one of the smartest financial decisions you can make in 2026.

Investing Your Tax Refund FAQ

Should I save or invest my tax refund?

Investing and saving your tax refund are both smart financial options, but the best choice for you depends on your personal situation. If you donŌĆÖt have an emergency fund, for example, putting your tax refund in a high-yield savings account for this purpose could be the best move. But if you already have some emergency savings, investing allows you to put your tax refund to work for your future.

Is it better to pay off debt or invest?

ItŌĆÖs almost always better to pay off high-interest debt than invest. For example, if you have credit card debt at a 21% APR, it doesnŌĆÖt make sense to invest in the stock market, which has historically returned about 10% annually. But if you only have low-interest debt, like mortgage debt, it can be a smarter idea to invest the money for your future.

How much of my tax refund should I invest?

Investing your tax refund can be a smart financial move, but the question of how much of your refund you should invest depends on your specific situation. For example, if you get a $3,000 tax refund but owe $1,000 on a credit card, it could be smart to pay off the credit card and invest the other $2,000.

What is the smartest thing to do with a tax refund?

The smartest thing to do with your tax refund is to use it in the way that best improves your financial well-being. Depending on your situation, this could mean using it to pay down credit card debt, build an emergency fund, or invest for your future.

Can I put my tax refund in a Roth IRA?

Yes, if you qualify to contribute to a Roth IRA, it can be an excellent way to use your tax refund. In 2026, the Roth IRA contribution limit is $7,500 ($8,500 if youŌĆÖre over 50), but the ability to contribute directly depends on your income, so be sure to check the Roth IRA income limits to make sure you qualify.

was produced by and reviewed and distributed by ┬ķČ╣įŁ┤┤.